What to Do with an Old 401(k) After You Leave a Job: 5 Options (and How to Choose)

Changing jobs comes with plenty to think about—new role, new benefits, new routines. But one money move often gets missed: what to do with your old employer’s 401(k).

The decision isn’t one-size-fits-all, but you generally have four main options—plus a fifth, Net Unrealized Appreciation (NUA), if you hold highly appreciated employer stock. Choosing well can help you reduce fees, simplify your finances, and keep your retirement plan on track.

Your Five Options at a Glance

- Leave it with your old employer—easy, but limited control.

- Roll over to your new employer’s 401(k)—simplifies management, if your plan allows it.

- Roll over to an IRA (Traditional or Roth)—wider investment choice and easier consolidation.

- Cash out—taxes and penalties usually make this a last resort.

- NUA strategy—a specialized tax move for appreciated employer stock.

Option 1: Leave Your 401(k) With Your Old Employer

What this means

You leave the money where it is. You can usually keep it invested and rebalance it, but you can no longer contribute.

Benefits

- No immediate action required—helpful during a hectic transition.

- Some large employers offer excellent, low-cost funds.

- Strong creditor protection in many cases (rules vary).

- You can roll it over later if you change your mind.

Drawbacks (fees are the big “silent” one)

- Fees vary widely—from roughly 0.87% to 3.56%¹—and small percentages compound into big dollars over time.

- Fees are often hidden in fund expense ratios, deducted silently from performance and easy to overlook — always check beyond the headline fee.

- Easy to lose track of (old logins, changing record keepers).

- You’re stuck with the plan’s investment menu.

- Loans typically aren’t available from old-employer plans.

- Possible “forced rollover” if your balance is small.

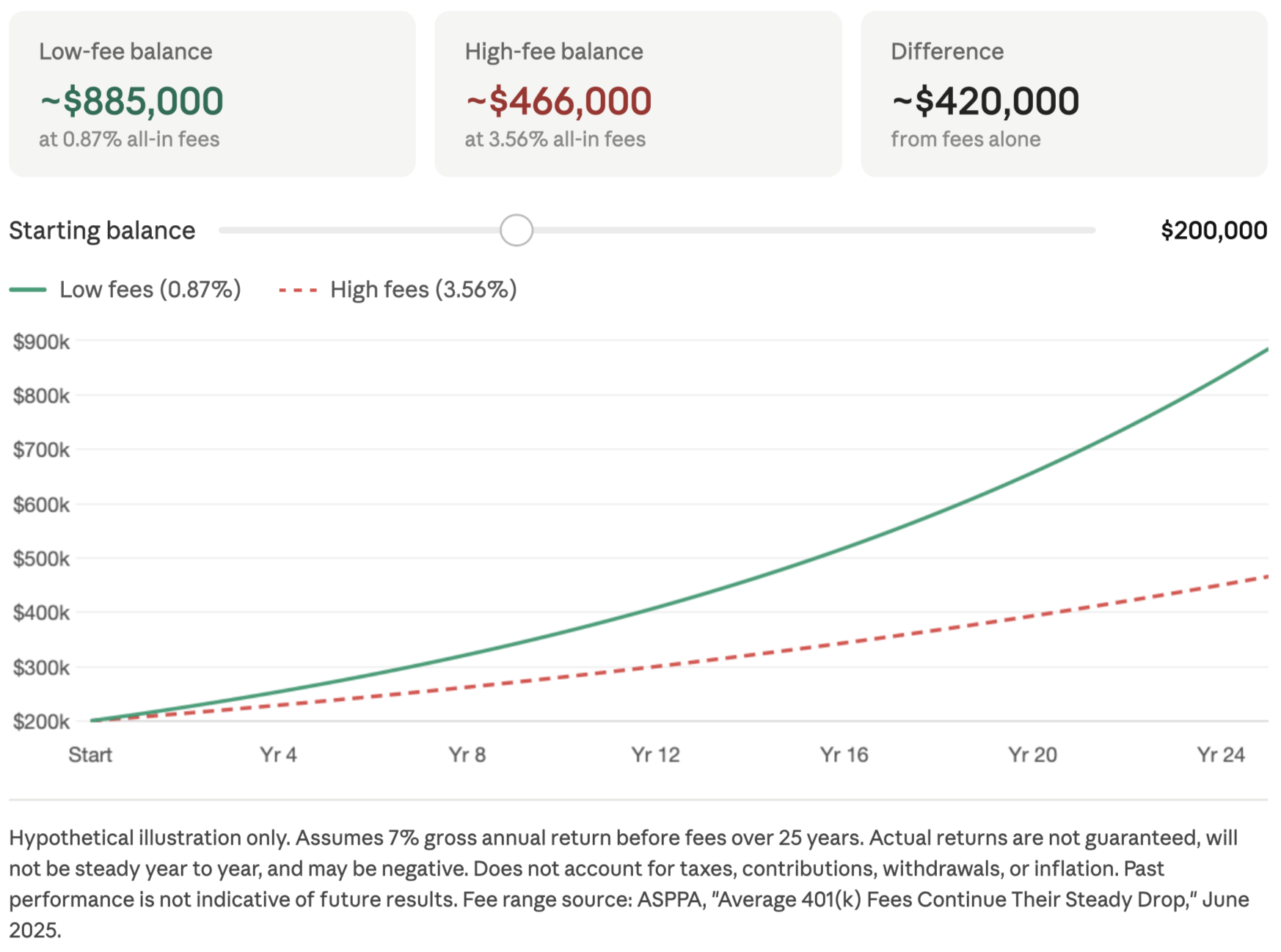

Fee impact example (hypothetical)

Say you have $200,000 in an old 401(k) and let it grow for 25 years at 7% per year before fees:

- At 0.87% in fees → grows to ~$885,000

- At 3.56% in fees → grows to ~$466,000

That’s a ~$420,000 difference—from fees alone, without adding a single extra dollar. (Returns aren’t guaranteed and won’t be steady every year, but the example shows why fees deserve attention.)

Best for: People whose old plan has low fees and good investment options, or those who want to delay a decision temporarily.

Option 2: Roll Over to Your New Employer’s 401(k)

What this means

If your new plan accepts rollovers, you can move your old balance in and consolidate your retirement savings under one roof.

Benefits

- Fewer accounts and passwords; easier rebalancing.

- Keeps money in a workplace plan, which can offer added legal protections.

- May preserve access to 401(k) loans (IRAs don’t allow them).

- Useful if you use a backdoor Roth IRA—keeping pre-tax money in a 401(k) avoids certain tax complications.

Drawbacks

- Your new plan may have higher fees or fewer investment options.

- Rollovers can take time (paperwork and processing).

- Less flexibility than an IRA—you’re limited to the plan’s menu.

Best for: People who value simplicity and have a strong new plan with competitive fees and good investment options.

Option 3: Roll Over to an IRA (Traditional IRA or Roth IRA)

What this means

When you roll an old 401(k) into an IRA, the goal is usually to keep the money in the same tax “bucket”:

- Pre-tax money typically rolls into a Traditional IRA.

- Roth 401(k) money typically rolls into a RothIRA.

- After-tax (non-Roth) employee contributions, if your plan tracks them, may roll into a Roth IRA—often paired with rolling the associated earnings into a Traditional IRA.

Done correctly, this rollover isn’t taxable—as long as it’s a direct rollover, or an indirect rollover completed within 60 days (more on that below).

Benefits

- Wide range of investment options (ETFs, index funds, etc.).

- Potentially lower costs and more transparent fees.

- Easy to consolidate multiple old retirement accounts over time.

- Can simplify Required Minimum Distributions (RMDs) by aggregating across IRAs and withdrawing the total from one account

- Qualified Charitable Distributions (QCDs): If you are charitably inclined and age 70½ or older, IRAs allow you to donate up to $111,000 in 2026 directly to a qualified charity — potentially $222,000 if married filing jointly — excluding the amount from taxable income and satisfying your RMD. This strategy is not available from a 401(k).

Drawbacks

- The pro-rata rule can complicate backdoor Roth contributions if you keep pre-tax money in a Traditional IRA.

- Creditor protection may be weaker than in a401(k) (varies by state).

- Roth conversions create a tax bill if you move pre-tax dollars into a Roth IRA.

- Loans aren’t available from IRAs.

Best for: People who want maximum investment choice, prefer managing retirement savings in one brokerage, and are comfortable with the tax planning involved.

Option 4: Cash Out Your Old 401(k)

What this means

You withdraw the money and take it as cash.

Benefits

- Immediate access to money (helpful in a true emergency).

- Simple—the account is closed and no longer needs managing.

Drawbacks (often the most expensive option)

- Taxes: withdrawals are generally taxed as ordinary income

- Potential 10% early withdrawal penalty if you’re under 59½ (some exceptions exist)

- You lose future compounding: cashing out can permanently set your retirement plan back

Best for: Usually a last resort—only after weighing alternatives and understanding the tax and penalty hit.

Option 5: NUA (Net Unrealized Appreciation)

What this means

NUA is a specialized tax strategy for appreciated employer stock held inside a 401(k).

How it Works

- You hold appreciated employer stock in your 401(k).

- You take the stock (not cash) as a lump-sum distribution.

- You pay ordinary income tax only on the original cost basis—not the appreciation.

- When you later sell the stock, the appreciation is taxed at long-term capital gains rates.

Benefits

- Tax Savings: potentially lower taxes on stock appreciation.

- Flexibility: take stock without an immediate full tax impact.

Considerations

- Complexity: the rules are intricate and easy to mishandle.

- Tax Implications: coordinate with a qualified professional before executing.

- Age: early withdrawal rates apply to the cost basis portion of a NUA distribution. If you are under the age of 59½, that amount is generally subject to a 10% early withdrawal penalty in addition to ordinary income tax. An exception exists under the Rule of 55 — if you separate from service in or after the year you turn 55, the 10% penalty may be waived on distributions from that employer's plan. The NUA appreciation itself is not subject to the early withdrawal penalty, but the cost basis is. Age and timing matter significantly in determining whether an NUA distribution makes financial sense.

Best for: Anyone with highly appreciated employer stock inside an old 401(k).

We’ll cover NUA in greater detail in a future post. If you have questions about the strategy or want personalized guidance, reach out to a Neptune Wealth advisor.

Direct vs. Indirect Rollovers

If you’re rolling money over, how you do it matters.

Direct rollover (usually easiest and safest)

A direct rollover (trustee-to-trustee transfer) moves funds straight from your old plan to your new 401(k) or IRA custodian. The check is typically made payable to the new custodian for your benefit—not to you. There’s no limit on how many direct rollovers you can do per year.

Why it’s preferred: it avoids tax withholding, missed deadlines, and accidental taxable events.

Indirect rollover (the 60-day rule applies)

With an indirect rollover, the money is paid to you first, and you then deposit it into an eligible retirement account. You’re limited to one indirect rollover in any 12-month period.

- The 60-day rule: You generally have 60 days from receipt to redeposit the funds. Miss it, and the IRS may treat it as a taxable withdrawal—plus a possible 10% penalty if you’re under 59½.

- The withholding trap: The plan may withhold taxes before sending you the money. To roll over the full amount, you may need to cover the withheld portion out of pocket when you redeposit.

Bottom line: if you want to keep retirement dollars in retirement accounts, a direct rollover is the cleanest path.

A Simple Decision Framework

Ask yourself:

- Is the old plan low-cost with good investment options? If yes, leaving it may be fine—at least for now.

- Is your new employer's plan strong and rollover-friendly? If yes, consolidating into the new 401(k) can simplify life.

- Do you plan to use a backdoor Roth IRA? If yes, be cautious about rolling pre-tax money into a Traditional IRA.

- Do you need cash now? If yes, weigh the tax and penalty cost—and explore alternatives first.

- Do you hold highly appreciated employer stock? If yes, consider the NUA strategy.

Before You Decide: A 2-Minute Checklist

Pull these details together first—they make the right answer much clearer:

- All-in fees in the old plan (admin fees + fund expense ratios).

- Quality of the plan’s investment options (low-cost index and target-date funds).

- Whether the old plan lets you keep your money there (some require minimum balances).

- Whether your new employer’s plan accepts rollovers.

- Whether you plan to use a backdoor Roth IRA in the future.

Have Questions About Your Old 401(k)? Contact Us.

If you’ve recently left a job—or have an old 401(k) you’ve never moved—reach out. We’ll help you understand your options, avoid common rollover mistakes, and choose a path that fits your bigger financial plan.

Important note: This article is for education only, not individualized tax or investment advice. Rules vary by plan and person—consider talking with a qualified professional. Past performance is not indicative of future results. Investing involves risk, including possible loss of principal. Neptune Advisory LLC (d/b/a Neptune Wealth) is a Registered Investment Adviser in Pennsylvania, Florida, and Wisconsin. Please review our Form ADV Part 2 and disclosures before engaging our services.

Sources

- ASPPA (American Society of Pension Professionals & Actuaries). “Average 401(k) Fees Continue Their Steady Drop.” June 2025.https://www.asppa-net.org/news/2025/6/average-401k-fees-continue-their-steady-drop/