Weekly Market Update: April 27 - May 1, 2026

Only a few weeks have ever packed as much into five sessions as this week has. An OpenAI bombshell rattled AI-linked names Tuesday, four Fed dissenters made history at a single meeting for the first time since 1992, Magnificent 7 earnings delivered massive beats that still triggered selling on capex anxiety, and a Friday rally powered by Apple's record quarter pushed the S&P 500 and Nasdaq to fresh all-time highs. April closed with strength and resilience.

What Happened This Week

All major indices closed higher on the week, with the Nasdaq leading the charge, gaining 1.41%, followed by the S&P 500 up 0.98%, the Russell 2000 up 0.60%, and the Dow rounding out the week with a modest gain of 0.43%

.png)

Three forces defined the week: an earnings season running well ahead of expectations, a Fed that delivered more drama than a "hold" typically warrants, and an OpenAI headline that tested theAI trade before the hyperscalers answered.

Tuesday — The OpenAI Shock (and the Courtroom)

A report surfaced that OpenAI had missed 2025 revenue and weekly active user targets, raising concerns about its ability to sustain massive infrastructure spending and likely pushing its anticipated IPO from late 2026 to late 2027. The report cited competitive pressure from Anthropic and Google's Gemini. OpenAI disputed it as "clickbait."

The headline landed alongside a noisier backdrop: the Musk v. Altman trial opened this week in federal court in Oakland, with Elon Musk seeking $130B in damages and a return of OpenAI to nonprofit status. The case won't resolve quickly, but it adds governance uncertainty around OpenAI specifically — even as the broader AI buildout thesis was decisively validated by hyperscaler results.

Wednesday — The Fed Holds, Four Dissenters

The Fed kept rates unchanged at 3.50%–3.75% for a third consecutive meeting — broadly expected. What was not expected was the level of internal division. Four members dissented (the most since 1992), with three officials (Logan, Hammack, Kashkari) opposing inclusion of an "easing bias" in the statement. The Fed also replaced "somewhat elevated" with "is elevated" in its inflation language — a meaningful hawkish shift — and cited Middle East developments and rising energy prices as contributors to a "high level of uncertainty."

Odds of a 2026 rate cut hit a fresh low. With inflation still above 3% and oil elevated, the Fed appears braced for more inflation, not preparing to ease. The 10-year yield held around 4.39%. This is also likely Jerome Powell's final meeting as Chair, with Kevin Warsh expected to take over — a transition the bond market will watch closely.

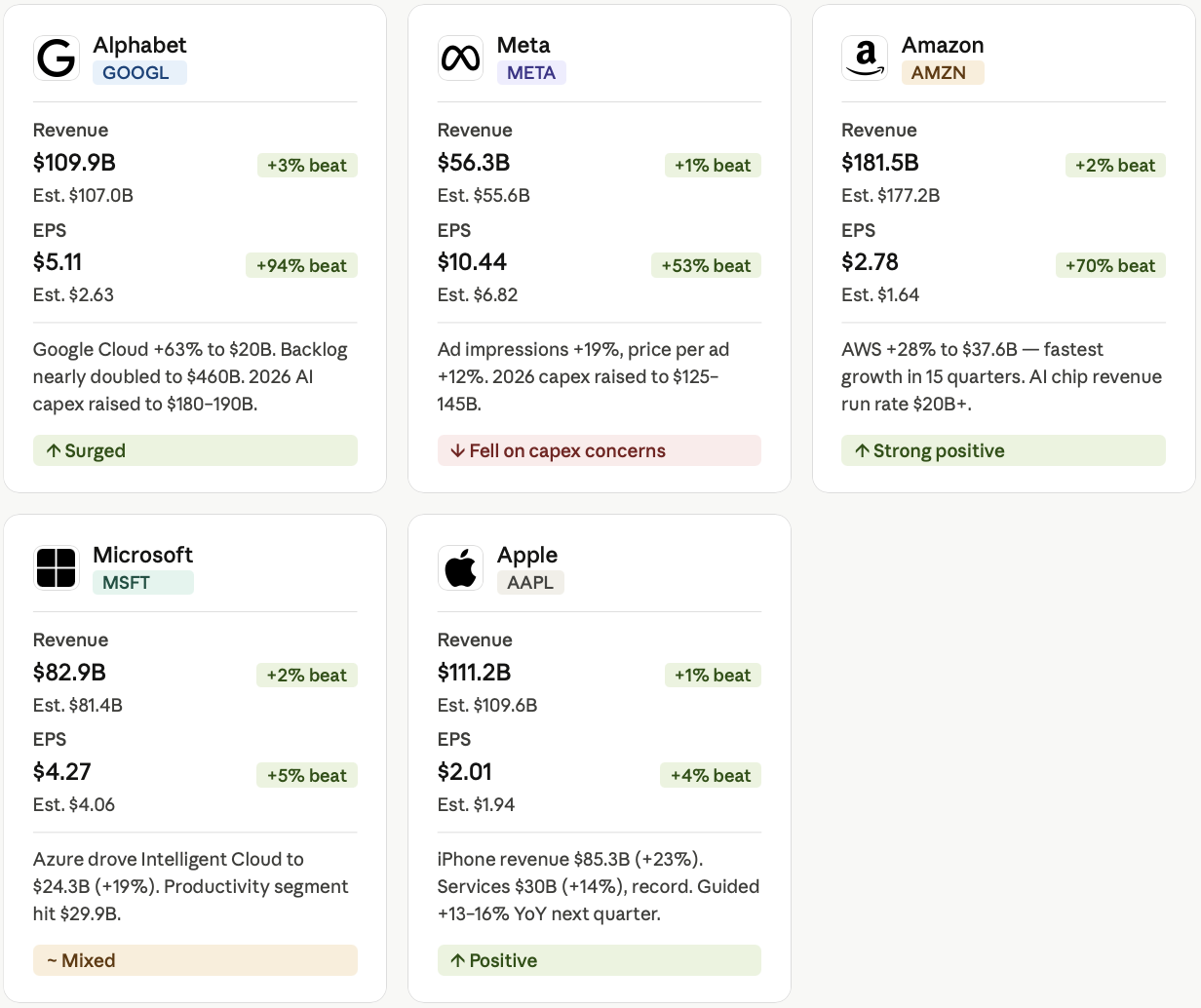

Wednesday/Thursday — Magnificent 7 Earnings

Five of the seven Magnificent 7 reported and delivered across the board. All five beat on revenue and EPS, and all five raised AI capex guidance. For some names, the question of when that spending converts to proportional returns triggered selling even as the underlying results were exceptional.

The theme is unprecedented AI capital commitment. Microsoft, Alphabet, Amazon, and Meta announced capex that is reshaping corporate America's capital allocation landscape. The ROI debate won't disappear — but cloud and enterprise AI revenue is beginning to answer it in real time. AWS growing at its fastest rate in 15 quarters is a data point, not a hypothesis.

Apple reported after Thursday's close and delivered its best-ever quarter. Markets responded Friday with a rally that lifted the Nasdaq and S&P 500 to new highs — capping a week that, despite a war, a contentious Fed meeting, and an OpenAI scare, finished at records.

The Earnings Picture

With nearly two-thirds of S&P 500 companies reported, 84% have beaten EPS estimates — the highest rate since Q2 2021 — with blended earnings growth of 27.1%, the strongest since Q4 2021. Nine of eleven sectors are reporting year-over-year growth. Communication Services, IT, and Consumer Discretionary are leading, driven primarily by Alphabet, Amazon, and Meta, which together accounted for 71% of the net increase in S&P 500 earnings this week. Analysts now project full-year 2026 earnings growth of 21.3%.

Geopolitics, Fed uncertainty, and OpenAI headlines all create volatility — but the earnings picture keeps coming in stronger than expected, providing a real floor beneath the market.

What We're Watching This Week

- Earnings: Palantir, AMD, Shopify, Uber, Snap, ARM, Coinbase, Airbnb, McDonald's, and Disney will test whether the strong earnings narrative can extend.

- Friday, May 8 — NFP, Unemployment, Michigan Sentiment: A weak print could revive rate-cut hopes; a strong one reinforces higher-for-longer.

- Oil: WTI pulled back to ~$101 Friday — constructive, but Middle East developments remain the primary driver.

- Kevin Warsh transition: Any early commentary will be parsed carefully.

- AI capex follow-through and OpenAI: Infrastructure suppliers (chips, power, connectivity, cooling) are the next leg of validation; OpenAI revenue and trial headlines will continue to move AI-complex sentiment.

The Bigger Picture

April ends near all-time highs — Nasdaq up more than 15% and S&P 500 up more than 10% for the month, among the strongest performances in years. The AI buildout is not slowing; it is accelerating, and this week's earnings proved it.

That said, with markets at records we remain cautious. The Fed is more divided than it has been in over three decades, inflation remains above 3%, oil stays elevated, and the Middle East ceasefire remains fragile. The fundamentals are real and we are positioned accordingly — but we are managing risk carefully and will keep you informed as conditions develop.

This market update is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

Our Form ADV Part 2, which describes our services, fees, conflicts of interest, and advisory practices in detail, is available at Form ADV Part 2 and at www.adviserinfo.sec.gov.

Educational content only. This article is for informational and educational purposes and does not constitute investment advice or a recommendation of any specific strategy or service. All references to AI tools describe general capabilities of technology in the financial services industry; they do not represent performance guarantees or specific results for any client. Past performance is not indicative of future results. Investing involves risk, including possible loss of principal. Neptune Advisory LLC (d/b/a Neptune Wealth) is a Registered Investment Adviser in Pennsylvania, Florida, and Wisconsin.. Please review our Form ADV Part 2 before engaging our services.