Weekly Market Update: April 20 - April 24, 2026

This was a week that had everything — a dramatic Sunday night headline, record highs mid-week, a Thursday pullback, and a Friday surge powered by one of the most surprising earnings beats of the season. Let us walk you through what happened, how we're thinking about it, and what we're watching heading into next week.

As always, feel free to read in full or jump to the sections most relevant to you.

What Happened This Week

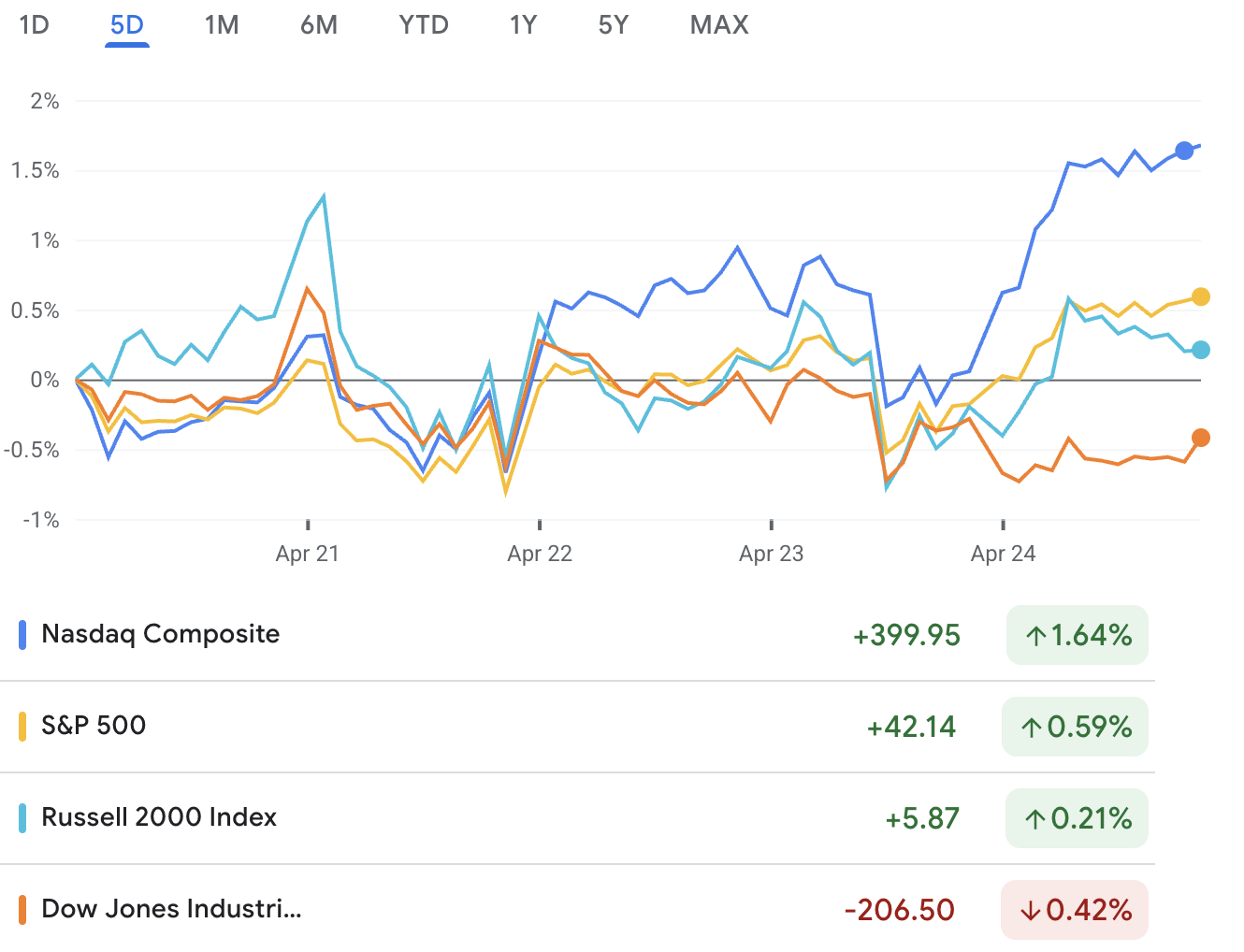

Markets finished the week meaningfully higher, with the S&P 500 and Nasdaq both closing at record levels on Friday. The S&P 500 ended the week at 7,165.08, while the Nasdaq closed at 24,836.60. The Dow finished at 49,230.71. The week's final tally represents a continuation of the broader recovery, with the S&P 500 having fully erased its Iran war losses and sitting at all-time highs.

Weekly performance across the major indices:

There were two defining forces this week — an earnings season running well ahead of expectations, and a geopolitical situation that continues to evolve, sometimes dramatically, day by day.

Sunday Night — U.S. Navy Seizes an Iranian Vessel

The week began with a significant headline before markets even opened. On Sunday evening, President Trump announced that the U.S. Navy had struck an Iranian ship transiting the Strait of Hormuz and that U.S. Marines had taken full custody of the vessel. It was an escalatory development that, in a different market environment, might have triggered a sharp risk-off move in futures.

Instead, markets absorbed it with notable composure. The underlying bid — built on strong earnings, improving geopolitical momentum, and investors who have already weathered weeks of turbulence — proved more resilient than the headline might have suggested. That resilience in the face of geopolitical shocks has become a defining characteristic of 2026’s market, and it continued this week.

Wednesday — Records and a Ceasefire Extension

The S&P 500 and Nasdaq both finished at record levels on Wednesday after President Trump extended the U.S. ceasefire with Iran, citing Tehran's "seriously fractured" government as the basis for the decision. Markets responded immediately. The combination of the ceasefire extension and a strong stream of earnings beats drove the S&P 500 to 7,137.90 and the Nasdaq to a new all-time intraday high.

Thursday — A Pause in the Rally

Stocks pulled back on Thursday, led by a drop in software stocks and a surge in oil prices, as uncertainty about the trajectory of the Iran war weighed on sentiment. The S&P 500 fell 0.41%, the Nasdaq declined 0.89%, and the Dow fell 0.36%.

On Thursday after the close, President Trump followed up with another announcement: the ceasefire between Lebanon and Israel has been extended by three weeks. While the near-term geopolitical picture remains fluid, the direction of travel continues to be constructive — and markets have learned to focus on direction rather than destination.

One-day pullbacks after significant run-ups are entirely normal. Thursday was a reminder that headline risk hasn't disappeared — it's simply being weighed against a very strong fundamental backdrop that continues to reassert itself.

Friday — Semiconductors & AI Infrastructure Lead

Intel's blowout Q1 results, driven by surging data center demand, sparked a broad market rally. The AI infrastructure buildout, encompassing data centers, power, connectivity, and cloud services, continues to drive growth. This expansion fueled significant gains in semiconductors and related sectors, contributing to a broad-based rally. Optimism extended beyond mega-cap tech, with enthusiasm for AI-driven growth trends evident across the market.

Intel’s print wasn’t just a win for one company — it was confirmation that enterprise and hyperscaler spending on AI infrastructure remains robust and ahead of expectations.

The Earnings Picture

The broader earnings season is running well ahead of expectations. With 28% of S&P 500 companies now having reported, 89% have beaten earnings per share estimates — well above both the 5-year average of 78% and the 10-year historical average. Technology companies are driving most of the upward estimate revisions, with analysts continuing to raise 2026 forecasts as AI-related spending shows no signs of slowing.

This is important context for understanding the market's resilience. Geopolitical events are creating volatility. But the underlying corporate earnings picture — the actual foundation of equity valuations — is largely coming in stronger than expected, and that is providing a floor beneath the market that short-term headlines cannot easily break through.

Notable earnings next week:

Next week is one of the most consequential earnings stretches of the year. Five Magnificent 7 companies report in a two-day window — Microsoft, Alphabet, Meta, Amazon, and Apple all reporting Wednesday and Thursday after the close. These five companies alone account for roughly a quarter of the total S&P 500 market cap, meaning a bad reaction in even one or two can drag the entire index lower regardless of what everything else does. The concentration risk cuts both ways.

The bull case is straightforward: all five beat, AI capex guidance holds or rises, and the Fed stays dovish — the Nasdaq surges and momentum across the portfolio ignites. The base case is mixed beats and neutral guidance, producing choppy stock-by-stock action rather than a broad move. The bear case — a miss or capex cut from one of the heavyweights, coupled with a hawkish Powell — hits growth stocks hardest and puts index support levels back in play. The earnings floor we’ve been building gets its most significant test next week.

The Bigger Picture

In early March, we were navigating the initial shock of military conflict in the Middle East. Today, we have major indices at all-time highs, an earnings season running well ahead of expectations, and a geopolitical situation moving — haltingly, non-linearly, but genuinely — toward resolution. That is a remarkable shift in a short period of time.

We are not dismissing the risks ahead. The ceasefire is fragile. Oil has not fully retreated and remains elevated at levels that bear watching for their impact on inflation expectations and consumer spending. The U.S.-Iran final deal remains unsigned. And in a market trading at elevated valuations, any meaningful disappointment in earnings or geopolitics could move prices quickly.

We believe the fundamental trends driving AI infrastructure growth are strong and enduring. Recent earnings, such as Intel's blowout print, confirm the ongoing investment in AI capabilities. This trend is expected to continue, with significant capital expenditures underway, making it one of the most substantial investment cycles in recent history. As the earnings season progresses, particularly with hyperscalers reporting soon, we can expect further validation of this growth narrative.

As always, please reach out with any questions or if you'd simply like to talk through your individual situation. That is what we are here for.

This market update is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

Our Form ADV Part 2, which describes our services, fees, conflicts of interest, and advisory practices in detail, is available at Form ADV Part 2 and at www.adviserinfo.sec.gov.

Educational content only. This article is for informational and educational purposes and does not constitute investment advice or a recommendation of any specific strategy or service. All references to AI tools describe general capabilities of technology in the financial services industry; they do not represent performance guarantees or specific results for any client. Past performance is not indicative of future results. Investing involves risk, including possible loss of principal. Neptune Advisory LLC (d/b/a Neptune Wealth) is a Registered Investment Adviser in Pennsylvania, Florida, and Wisconsin.. Please review our Form ADV Part 2 before engaging our services.