Weekly Market Update: May 4 - May 8, 2026

It was a great week for equity investors. Markets pushed deeper into record territory: the Dow Jones Industrial Average crossed 50,000 for the first time since its February peak, and the S&P 500 and Nasdaq closed at fresh all-time highs. A blowout April jobs report on Friday and a sharp drop in oil prices on Iran peace-deal optimism powered the move, even as a brief Thursday pullback and a fresh Strait of Hormuz incident reminded investors how quickly the narrative can shift. So far, the "sell in May and go away” crowd has had a rough start to the month.

What Happened This Week

.png)

Three storylines defined the week: oil tumbled on peace-deal hopes before bouncing on a fresh Hormuz exchange, an April jobs report came in nearly twice consensus, and the Senate machinery put Kevin Warsh on track to be confirmed Fed Chair within days.

Friday — Jobs Blow Past Expectations

The April employment report delivered the week's biggest surprise. Nonfarm payrolls rose 115,000, well above the ~62K consensus, with unemployment steady at 4.3%. March was revised up to +185K and February down to -156K. Wages rose 0.2% on the month (+3.6% YoY) — firm but not accelerating. Gains were led by health care (+37K), transportation and warehousing (+30K), and retail trade (+22K), while federal government employment continued to decline (-9K).

Markets read the report as a "low-hire, low-fire" Goldilocks print — enough strength to keep recession concerns off the table, not so hot as to revive aggressive rate-hike pricing. Friday's session saw the S&P 500 add 0.84%, the Dow gain 0.02%, and the Nasdaq rise 1.71%, with both broad indexes setting fresh records.

The Oil Reversal — and a Reminder It Remains Fragile

Energy was the story of the early week. Brent and WTI both fell sharply on reports the U.S. and Iran were closing in on a 14-point memorandum of understanding to formally end the war, reopen the Strait of Hormuz, place a moratorium on Iranian nuclear enrichment, and unwind sanctions in stages. Oil dropped more than 7% earlier in the week, pulling Treasury yields lower and supporting equity multiples broadly.

Friday brought a reminder of the geopolitical premium still in this market: U.S. and Iranian forces exchanged fire in the Strait of Hormuz overnight, threatening the fragile ceasefire that has held since April 8. Brent rebounded 2.6% to ~$102.70 and WTI rose 2.0% to ~$96.66, though both ended the week meaningfully below where they started. We are watching the next round of negotiations closely.

Powell-to-Warsh Transition Clears Its Final Hurdle

The Senate Banking Committee advanced Kevin Warsh's nomination 13–11 along party lines — the first fully partisan committee vote on a Fed Chair nominee in U.S. history. Senator Tillis dropped his hold after the DOJ closed its investigation into Chair Powell. The full Senate vote is expected the week of May 11, with Warsh likely confirmed before Powell's term expires May 15. Powell will remain on the Fed Board for "a period of time to be determined." Markets have absorbed the change without disruption, but the new Chair's first FOMC will be closely watched for any signal of a shift in reaction function.

The Earnings Picture

With nearly 90% of S&P 500 companies now reporting, 84% have beaten EPS estimates and 80% have exceeded revenue forecasts — blended earnings growth is tracking near 28% year over year, the highest since Q4 2021. The forward 12-month P/E sits at 21x, above both the 5-year average of 19.9x and the 10-year average of 18.9x — a reminder that this market is priced for continued execution. So far, corporate America is delivering. The earnings floor beneath this market is real, and it has held through a week that offered no shortage of reasons to sell. Worth watching: Thursday's sharp rotation into software names may be an early signal that the AI value chain is beginning to broaden — from the infrastructure picks-and-shovels trade toward the application layer that runs on top of it.

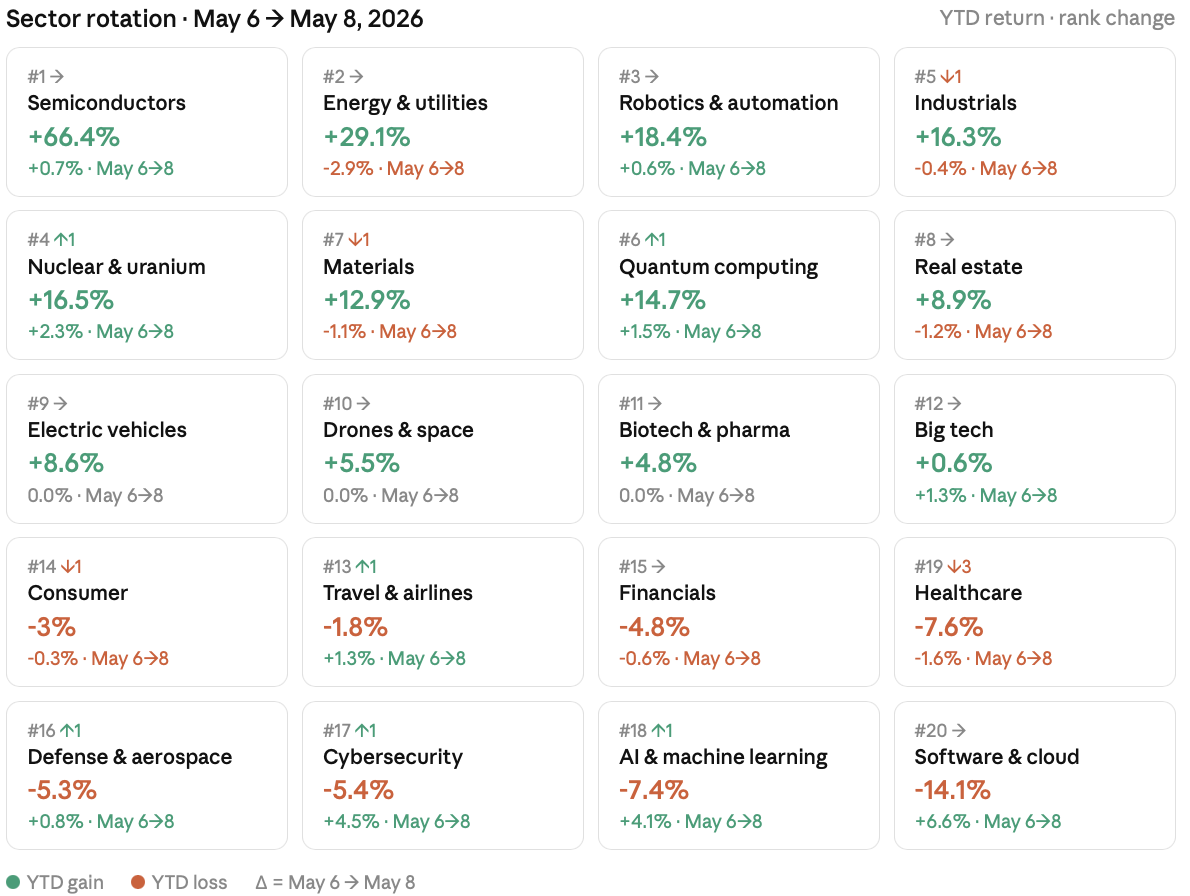

Sector Rotation in Focus

Between Wednesday and Friday, we saw significant inflows into sectors hit hardest this year. Energy and utilities saw the highest outflows (-2.9%), while software & cloud — the worst-performing sector YTD — saw +6.6% inflows. We expect this rotation into software to continue.

Three catalysts could extend this rotation:

- Fed pivot signal — growth and rate-sensitive sectors (Software, AI, Big Tech, Healthcare) re-rate higher immediately.

- Trade deal or tariff rollback — removes the uncertainty premium weighing on tech-adjacent names.

- Soft-landing confirmation — CPI plus jobs data showing controlled inflation without recession, pulling money from defensive winners (Semis, Energy) into beaten-down growth.

What We're Watching Next Week

- Senate Warsh vote: Final Senate vote expected the week of May 11. The Powell era formally ends May 15.

- April CPI (Tuesday, May 12): First inflation read of the spring. Energy moves will weigh on the headline; core will be the more informative number for the Fed.

- Earnings: Cisco, Alibaba, Applied Materials, Nebius, Sea Limited, and Constellation Energy headline a deep bench. AMAT in particular will be watched as a barometer for semiconductor equipment demand and the AI capex cycle.

- Iran/Hormuz: Negotiations on the 14-point MOU continue. Any escalation or breakthrough will move oil and risk assets immediately.

The Bigger Picture

It was an unusually positive setup: jobs strong but not too hot, oil down sharply on peace-deal momentum, earnings broadly holding up, and the Fed leadership transition proceeding without market disruption. Records are records — but with the Dow near 50K, Nasdaq and S&P at all-time highs, and a ceasefire that remains a Friday-headline away from breaking, we continue to manage risk carefully and stay alert to asymmetric tail risks.

Bull markets don't die of old age — they die because something kills them. The earnings are real, the labor market is resilient, and the AI buildout is accelerating. As always, please reach out with any questions about how these developments may affect your portfolio.

This market update is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

Our Form ADV Part 2, which describes our services, fees, conflicts of interest, and advisory practices in detail, is available at Form ADV Part 2 and at www.adviserinfo.sec.gov.

Educational content only. This article is for informational and educational purposes and does not constitute investment advice or a recommendation of any specific strategy or service. All references to AI tools describe general capabilities of technology in the financial services industry; they do not represent performance guarantees or specific results for any client. Past performance is not indicative of future results. Investing involves risk, including possible loss of principal. Neptune Advisory LLC (d/b/a Neptune Wealth) is a Registered Investment Adviser in Pennsylvania, Florida, and Wisconsin.. Please review our Form ADV Part 2 before engaging our services.