Weekly Market Update: May 25 - May 29, 2026

This week felt like two markets in one. The first half was all about chips and AI infrastructure — the picks-and-shovels names that have powered the rally for months — with Micron doing most of the headline work. The second half shifted: software stocks finally caught a bid after blowout earnings and a softer inflation reading began to chip away at one of the most stubborn worries hanging over this year’s market — the fear that AI was killing the software business rather than supercharging it.

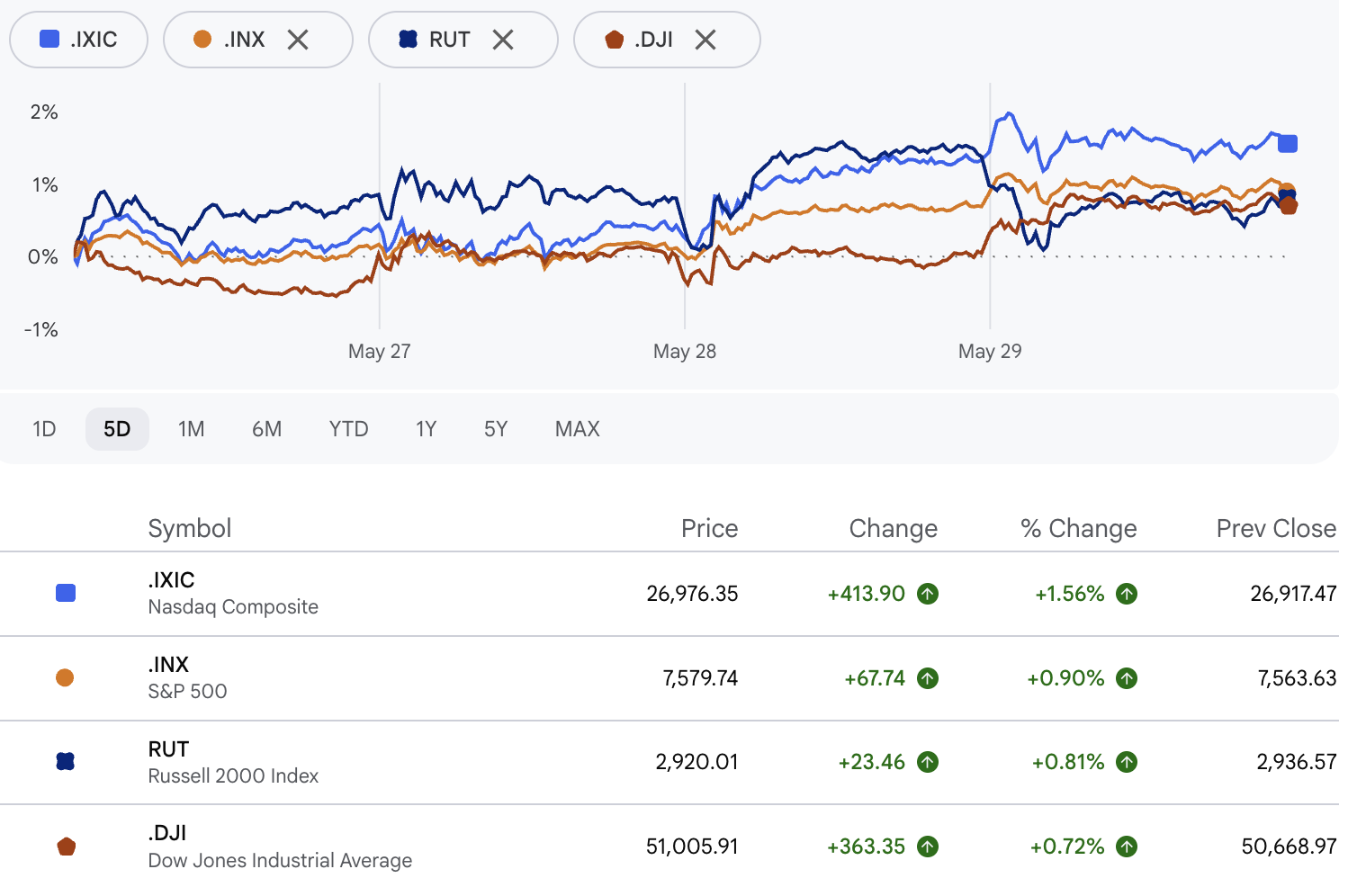

Underneath all of it, the U.S.–Iran situation continued to simmer, with limited military activity and ongoing ceasefire talks running side by side. Despite all of that, the S&P 500 and Nasdaq closed at fresh record highs on Friday, stretching the S&P’s winning streak to nine straight weeks. The market’s ability to climb a “wall of worry” — the old Wall Street phrase for shrugging off bad news — is on full display right now.

As always, feel free to read in full or skip to whatever section is most relevant to you.

What Happened This Week

Tuesday — The Chip Rally Keeps Rolling

Micron (MU) jumped 19% in a single session and crossed $1 trillion in market value for the first time in its history, after a UBS analyst nearly tripled his price target on the stock — from $535 to a Street-high $1,625. The thinking behind the call: roughly 30% of the industry’s DRAM memory supply is getting locked into long-term contracts. In plain English, the chips that AI systems rely on to remember and process information are now being sold the way oil and gas are — on multi-year agreements at set prices — which gives Micron a much more predictable earnings stream than it has ever had.

AMD also moved higher on the broader AI momentum. As we noted last week, memory is one of the biggest bottlenecks in the AI buildout — there simply isn’t enough of it being made fast enough — and that supply pressure is a core reason we hold a dedicated DRAM position inside our ETF portfolios.

Wednesday — Strikes in Iran, Markets Hold Steady

The U.S. military shot down four Iranian attack drones and struck a ground control station near Bandar Abbas, on Iran’s southern coast. The strikes were characterized by the Pentagon as limited and defensive — a response to a specific threat against U.S. forces and commercial shipping in the Strait of Hormuz, the narrow waterway that handles roughly 20% of the world’s oil trade. At a Cabinet meeting the same day, President Trump made clear the Strait will remain open to all traffic: “Nobody is going to control it.”

Markets barely flinched. That kind of calm reaction is itself a signal: investors have already priced in a meaningful amount of Iran-related risk, so individual headlines no longer move the dial the way they did earlier this year.

Thursday — Software’s Comeback, Inflation Data, and a Rocket Explosion

Thursday was the most important session of the week. A lot happened at once.

Snowflake reset the software conversation.

Snowflake — a cloud data and analytics company — reported quarterly revenue of $1.39 billion, up 33% year-over-year and well above the $1.32 billion analysts expected. Product revenue grew 34%. The company also announced a $6 billion partnership with Amazon Web Services to help large enterprises adopt AI more quickly. The stock jumped roughly 38% on the report. The bigger takeaway: for most of this year, investors have worried that AI would replace traditional software — why pay for a subscription when an AI agent can do the same job? Snowflake’s results pushed back on that fear hard. Software companies that build AI directly into their products are generating new revenue, not losing existing customers.

Anthropic raised the largest private AI round ever.

On the same day, Anthropic announced a $65 billion funding round at a $965 billion valuation — the largest private AI raise on record — alongside the release of its new Claude Opus 4.8 model. Paired with Snowflake’s report, the message landed clearly: AI is producing real, paid-for enterprise value, and the market is finally starting to reward the companies delivering it.

Inflation came in slightly cooler than expected.

The Fed’s preferred inflation gauge — known as core PCE — rose 0.2% in April, a touch below the 0.3% economists had penciled in. Year-over-year, core PCE was up 3.3%, in line with expectations but still nearly double the Fed’s 2% target. Energy costs are doing most of the work to keep that annual number elevated, largely tied to the disruptions in the Strait of Hormuz. The softer monthly figure gave small-cap stocks a lift on hopes that the Fed could cut rates sooner, while the annual reading kept the “higher for longer” rate narrative alive.

Diplomatic progress on Iran.

U.S. and Iranian negotiators reportedly reached a 60-day memorandum of understanding to extend the ceasefire and open direct talks on Iran’s nuclear program. The deal was still awaiting President Trump’s final sign-off as of week’s end, and Iran had not formally confirmed its acceptance — so the news is meaningful, but not yet final.

Blue Origin’s New Glenn rocket exploded.

Late Thursday night, Blue Origin’s New Glenn rocket exploded on the launch pad at Cape Canaveral during a pre-flight test. No one was hurt, but the vehicle was destroyed and the launch facility was damaged. Blue Origin has only one New Glenn pad, which means the timeline for launching Amazon’s Leo satellite network just got pushed back meaningfully. Space stocks sold off on Friday in response — a reminder that commercial spaceflight is still a very high-risk business.

Friday — Records, Software Keeps Running, Iran Still Open

Software stocks extended their move higher. The Dow crossed 51,000 for the first time ever, led by technology and financial names. Dell soared roughly 33% after reporting strong AI-related server sales. President Trump met with advisors in the Situation Room on the Iran deal but left without making an announcement. The ceasefire is still holding — at least for now.

What We Are Watching Next Week

The Iran memorandum of understanding is the single biggest variable. A signed deal would likely mean lower oil prices, a softer inflation outlook, and some relief for interest-rate-sensitive parts of the market. A breakdown would put the fragility of the ceasefire right back in the headlines.

On the data side, two key labor market reports land next week. JOLTS — a monthly survey of job openings — comes out Tuesday, and the more closely watched non-farm payrolls report (which tells us how many jobs the economy added) along with the unemployment rate comes out Friday. Together they will tell us whether the labor market is cooling in a way that might change the Fed’s thinking on rate cuts. A strong jobs print keeps cuts off the table; meaningful weakness could give software stocks more room to run.

Earnings will be the main event for us. CrowdStrike, Palo Alto Networks, C3.ai, and DocuSign all report — and collectively, they will tell us whether Thursday’s software repricing is the start of something bigger or a one-week story. If these names show the same revenue acceleration that Snowflake did, the bull case for our IGV position gets meaningfully stronger. Broadcom also reports and deserves attention on its own: as a supplier of networking gear and custom AI chips to the largest tech buyers, its forward guidance gives us a real-time read on whether enterprise AI spending is still accelerating.

The Bigger Picture

The AI trade is maturing. The first phase of the rally was concentrated in the infrastructure layer — the chips, power generation, and data centers that make AI possible. What this week suggested is that the next leg may come from the application layer: enterprise software companies that embed AI directly into the tools businesses already use every day. The long-running “AI will kill software” narrative is starting to show real cracks, and the companies actually delivering AI revenue are getting rewarded for it.

The tension between strong AI-driven fundamentals and a still-challenging interest rate environment is not going away. But for clients positioned across both the infrastructure and application layers of the AI buildout, this week was real-world confirmation that the underlying thesis is intact.

As always, please reach out with any questions about how any of this applies to your portfolio. That is what we are here for.

This market update is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

Our Form ADV Part 2, which describes our services, fees, conflicts of interest, and advisory practices in detail, is available at Form ADV Part 2 and at www.adviserinfo.sec.gov.

Educational content only. This article is for informational and educational purposes and does not constitute investment advice or a recommendation of any specific strategy or service. All references to AI tools describe general capabilities of technology in the financial services industry; they do not represent performance guarantees or specific results for any client. Past performance is not indicative of future results. Investing involves risk, including possible loss of principal. Neptune Advisory LLC (d/b/a Neptune Wealth) is a Registered Investment Adviser in Pennsylvania, Florida, and Wisconsin.. Please review our Form ADV Part 2 before engaging our services.