Weekly Market Update: June 1 - June 5, 2026

This was a week that ended very differently than it started. A brief flash of geopolitical calm gave way to a sharp reversal: Iran suspended nuclear talks, oil pushed back above $97 a barrel, and a blowout May jobs report on Friday forced markets to confront the possibility of a Fed rate hike before year-end — a scenario that was barely on anyone's radar a short while ago. Mixed earnings from two closely watched names (CrowdStrike and Broadcom) added another layer of complexity.

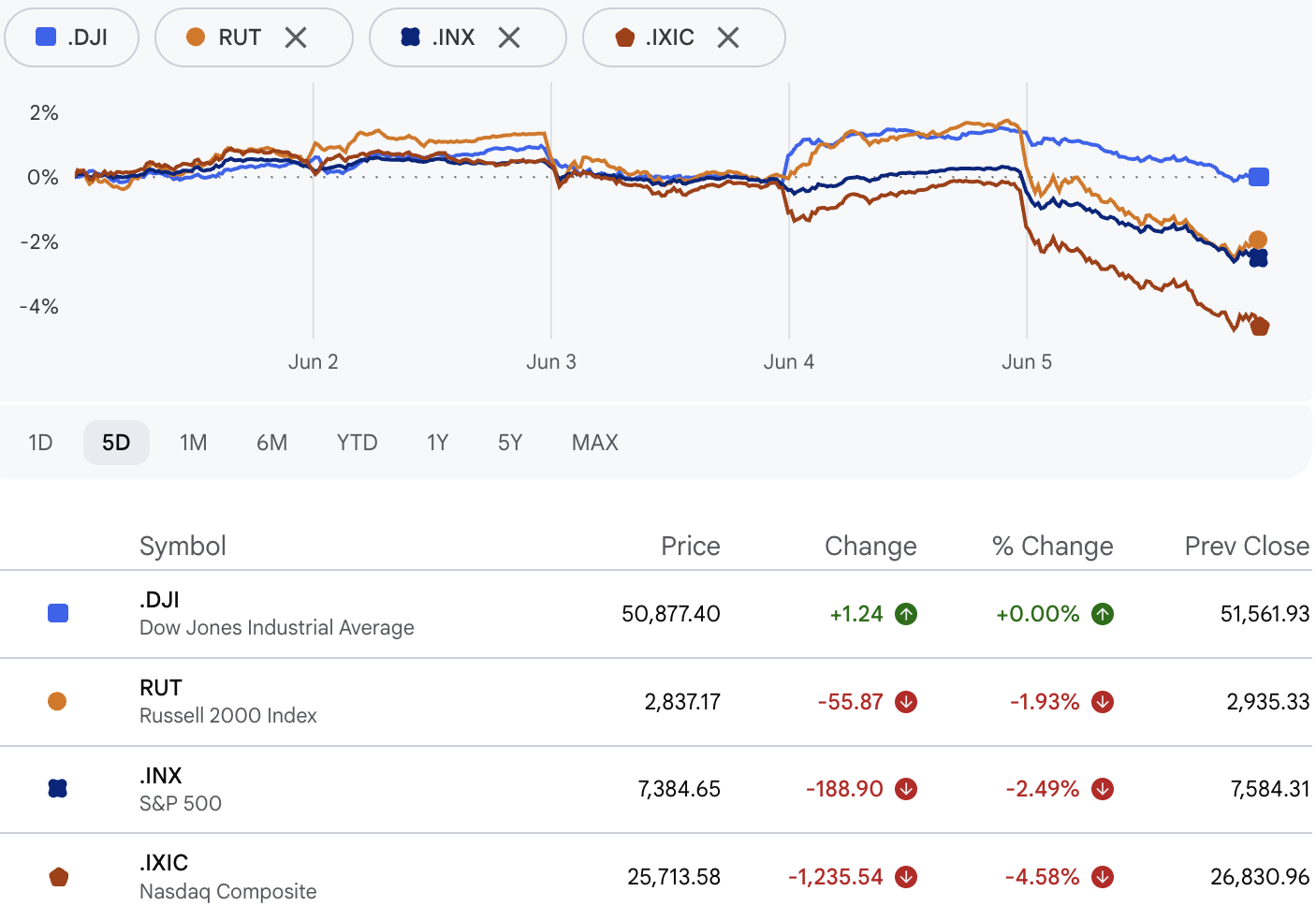

The week's net result: the S&P 500's ten-session daily winning streak ended on Wednesday, and by Friday the index had given back what it had gained early in the week — and then some — also snapping a multi-week green run. After weeks of seemingly shrugging off every piece of bad news, the wall of worry finally won one.

What Happened This Week

Monday — Oil Tops $97, Tech Holds the Line

The week opened with a jolt. Iran suspended its nuclear talks with the United States, citing Israel's expanding military operations in Lebanon, and Iran's semi-official Tasnim news agency raised the possibility of a full closure of the Strait of Hormuz. That was enough to send crude oil back above $97 per barrel and inject a fresh wave of uncertainty into a market that had been in a remarkably settled mood.

For the day, the broad indices finished mixed. AI-related technology names were strong enough to keep the Nasdaq in the green, but non-tech sectors — which are more directly exposed to higher energy costs and the rate pressure that tends to follow — pulled the Dow lower. The bifurcation between AI-driven tech and the rest of the market, a theme we have highlighted in recent updates, was very much on display.

Tuesday — Job Openings Surge, Geopolitics Heats Up

The JOLTS report — the government's monthly survey of job openings — came in hot. April openings jumped 731,000 to 7.62 million, well above the 6.8 million economists had expected and the highest level since November 2024. It was a meaningful signal that the labor market remains tight despite months of higher interest rates. A strong jobs market complicates the Federal Reserve's calculus: it reduces the urgency to cut rates and keeps the "higher for longer" narrative firmly in play.

Geopolitical headlines continued to escalate, with reports of an Iranian strike on military positions in Kuwait. While markets largely absorbed the news without a dramatic reaction, it reinforced the message from Monday: the recent ceasefire is increasingly fragile, and the risk premium in oil is not going away quickly.

Wednesday — A Red Day, and Two Big Earnings After the Close

Wednesday broke the S&P 500's ten-session winning streak with its first red close in nearly two weeks. The catalysts: oil continued to climb, the ADP private payroll report came in stronger than expected, Treasury yields moved higher in response, and the market's pricing of Fed rate cuts pushed further out on the calendar.

Two high-profile earnings reports — CrowdStrike and Broadcom — landed after the close. Both beat estimates, and both sold off anyway. In a market priced for perfection, that is exactly what tends to happen. Neither name is held in our All-Cap Strategies, but the reaction was telling.

CrowdStrike delivered a solid quarter.

Revenue came in at $1.39 billion, up 26% year-over-year, with adjusted EPS of $1.10 — both ahead of expectations. Annual recurring revenue reached $5.51 billion, up 24%, and net new ARR grew 32% to a record $256 million. The company also announced a 4-for-1 stock split, with the record date set for June 25 and split-adjusted trading beginning July 2. Full-year guidance was raised across revenue, ARR, and EPS, and management framed CrowdStrike as increasingly critical AI security infrastructure. The stock still sold off — not because the results were bad, but because the bar had been set impossibly high. Record ARR and a stock split were not enough when the market had already priced in something closer to perfection.

Broadcom beat on the headline but disappointed on what matters most.

Revenue came in at $22.2 billion, up 48% year-over-year, and adjusted EPS of $2.44 rose 54% — both ahead of estimates. The AI semiconductor segment grew 143% year-over-year to $10.8 billion. The problem: that AI number came in below the whisper expectations circulating on the buy side, and management's Q3 AI guidance of $16 billion (a +200% YoY growth rate) fell short of the $17+ billion analysts had been penciling in. Broadcom also did not raise its full-year AI revenue outlook — a meaningful omission in a market accustomed to "beats and raises" at every turn. Add in commentary around margin pressure as custom AI processors become a larger share of the mix, and investors had enough reasons to sell the news. The stock fell roughly 3% in extended trading and continued lower through the week.

Thursday — A Quiet Respite

Stocks bounced. Value names and financials led the way as Broadcom's gravity continued to weigh on the broader tech complex. Initial jobless claims came in at 225,000, slightly above the 213,000 estimate — a modest sign that the labor market may be cooling at the margin. Oil prices pulled back from their highs, providing some relief for rate-sensitive parts of the market. It was not a dramatic session, but after Wednesday's pressure it felt like a necessary exhale.

Friday — The Jobs Report Changes the Conversation

Nobody saw the May payrolls report coming. The economy added 172,000 jobs in May, more than double the 80,000 economists had forecast. The unemployment rate held steady at 4.3%. Equally important, March and April were both revised meaningfully higher — March to +214K (a 29K upward revision) and April to +179K (a 64K upward revision). Average hourly earnings rose 0.3% on the month and 3.4% year-over-year. Gains were led by leisure and hospitality (+70K), local government (+55K), health care (+35K), and manufacturing (+7K).

Treasury yields surged on the print, and by Friday afternoon markets were pricing in the possibility of a Fed rate hike by year-end — a dramatic reversal from the rate-cut expectations that had dominated the conversation just weeks ago. All major indices fell sharply, with the tech-heavy Nasdaq leading the decline. The combination of higher oil prices, a labor market that refuses to cool, and the prospect of tighter monetary policy is not a friendly environment for equities priced at current valuations. It was a meaningful reminder that the macro backdrop remains fragile, and that a single data point can reshape the narrative in a hurry.

What We're Watching Next Week

- May CPI (Wednesday, June 10) and PPI (Thursday, June 11): Together they will tell us whether Friday's jobs shock is part of a broader re-acceleration in inflation or an outlier. After two consecutive hot inflation prints already in this cycle, CPI is the single most important data point of the week — and the most important read on whether the Fed will stay on hold, cut, or be forced toward a hike.

- Oracle earnings (Wednesday, June 10): Reporting after the close. As one of the largest enterprise software and cloud-infrastructure businesses in the world, Oracle's forward guidance will offer a real-time read on whether enterprise AI spending is still accelerating — particularly relevant given our IGV position in the ETF strategies and the broader software re-rating thesis we have been building around.

- The Warsh Fed: Kevin Warsh has been Fed Chair since May 22, and his "old-fashioned" definition of inflation — paraphrased as "price stability is a state in which no one is talking about prices" — sets a noticeably higher bar than the prior 2% framework. Any commentary out of the Chair or other governors next week will be scrutinized for how a Warsh-led Fed plans to read Wednesday's CPI print.

- Iran and the Strait of Hormuz: Suspended talks are not the same as a broken ceasefire, but the two can feed each other quickly if the Lebanon conflict expands. Any move toward a Hormuz closure — even a threatened one — would send oil materially higher and complicate the Fed's path considerably.

- Treasury yields: After Friday's spike, bond-market stability will be important for equity-multiple support heading into the week. Continued pressure on yields would remain a headwind, particularly for longer-duration growth names.

The Bigger Picture

The AI spending cycle is intact — Broadcom's 143% year-over-year AI semiconductor growth is not a number that suggests anything other than an arms race still in full swing. But the market's reaction to Broadcom's quarter is a useful data point about where we are in the sentiment cycle: when 143% growth disappoints because something closer to 160% was expected, we are operating at multiples where the margin for error is thin.

That is not a reason to abandon the AI thesis. It is a reason to be precise about where we are positioned within it, disciplined about valuations, and willing to hold cash when the right opportunities have not yet presented themselves. It is also why we have been systematically trimming our biggest winners over the past several weeks — not from a lack of conviction, but because locking in gains and managing concentration risk at stretched valuations is what disciplined portfolio management looks like in practice. This week's macro developments only reinforced that instinct.

We also want to say this directly: weeks like this one are never fun, and we know that. It is worth remembering, though, that a long run of weekly gains in the S&P 500 is a remarkable streak by any historical standard — and a pullback after a move like that is not just normal, it is healthy. Markets need to digest gains, reset expectations, and shake out excess before the next leg higher can begin. We work hard to balance growth with risk mitigation, and trimming winners, raising cash, and rotating into more defensive positioning are all part of how we do that. Volatility is part of investing, and no matter how carefully we manage the portfolio, difficult weeks can and do happen along the way. If you are ever uncomfortable with the level of volatility you are experiencing, or simply want to talk through how your portfolio is positioned, please do not hesitate to reach out. That is exactly what we are here for.

This market update is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

Our Form ADV Part 2, which describes our services, fees, conflicts of interest, and advisory practices in detail, is available at Form ADV Part 2 and at www.adviserinfo.sec.gov.

Educational content only. This article is for informational and educational purposes and does not constitute investment advice or a recommendation of any specific strategy or service. All references to AI tools describe general capabilities of technology in the financial services industry; they do not represent performance guarantees or specific results for any client. Past performance is not indicative of future results. Investing involves risk, including possible loss of principal. Neptune Advisory LLC (d/b/a Neptune Wealth) is a Registered Investment Adviser in Pennsylvania, Florida, and Wisconsin.. Please review our Form ADV Part 2 before engaging our services.