Weekly Market Update: June 8 - June 12, 2026

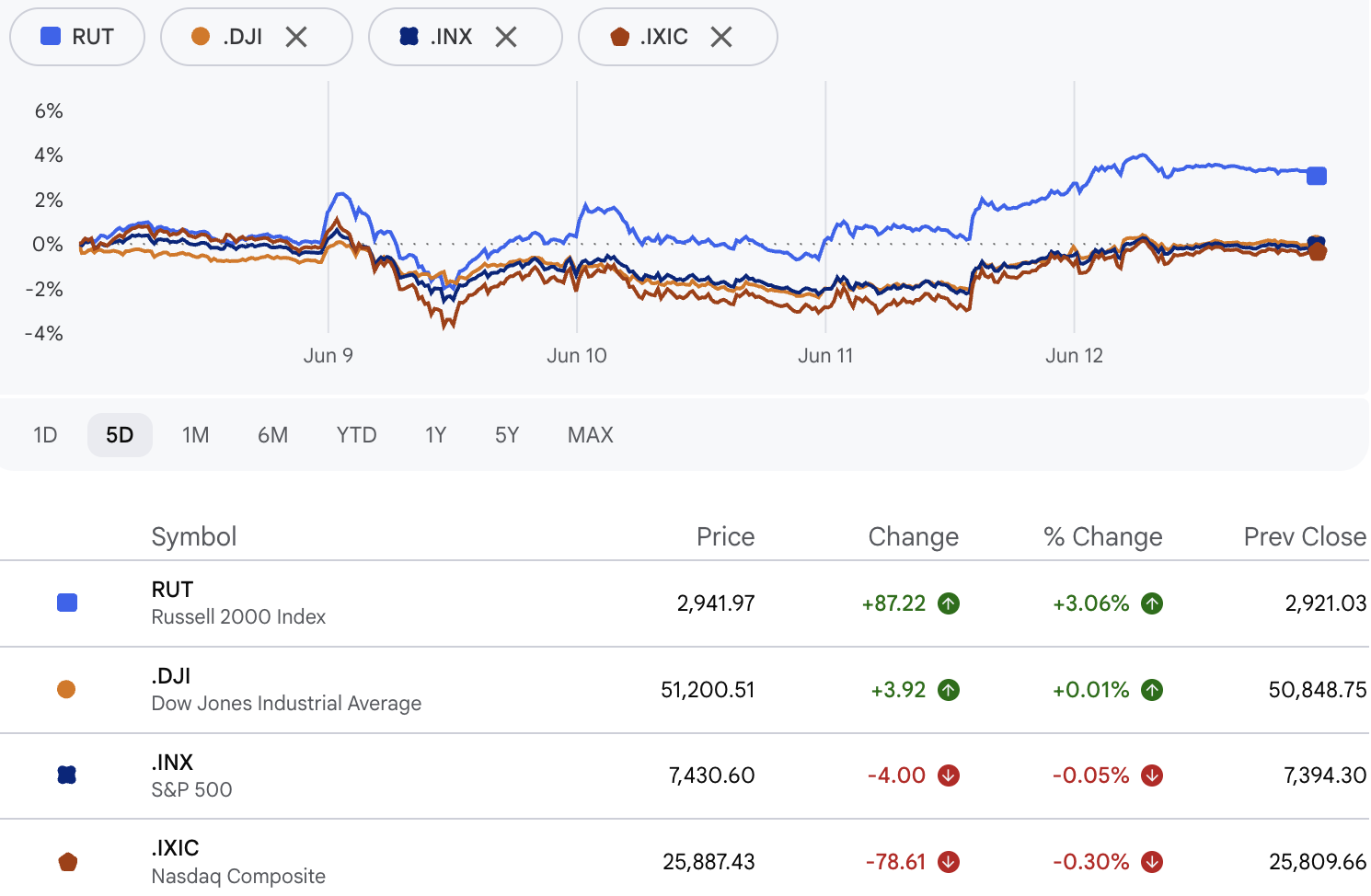

It is hard to remember a week with as much movement, in as many directions, as this one. We came in off a sharp Friday selloff and ran straight into a weekend missile exchange between Israel and Iran. From there, every single session brought something significant: a major tech rebound on Monday, a 5% intraday plunge and substantial recovery on Tuesday, a hot CPI print on Wednesday, a complete reversal on Iran by Thursday afternoon, and on Friday, the largest IPO in history. The time between a steep selloff and a meaningful recovery was often measured in hours rather than days.

We want to walk you through what happened, what we did about it, and what we are watching from here. As always, feel free to read in full or skip to what is most relevant to you.

What Happened This Week

Over the Weekend — The Ceasefire Cracks

On Sunday, Iran launched missiles at Israel — the first such exchange since the fragile ceasefire that took effect on April 8. The strikes came hours after Israel bombed a Hezbollah command headquarters in Beirut’s southern suburbs, which Israel described as retaliation for Hezbollah firing toward northern Israel. Markets had closed Friday assuming the ceasefire was holding. They reopened Sunday evening to a different picture entirely.

Monday — Tech Rebounds, OpenAI Files for IPO

Given how serious the weekend headlines were, Monday’s market reaction was surprisingly measured. Technology and chip stocks recovered meaningfully from Friday’s selloff, with investors deciding the weekend exchange did not fundamentally change the longer-term path of the conflict. Trump said Monday that both sides were looking for an immediate ceasefire and that peace negotiations were continuing, which helped settle nerves.

The day’s other headline: OpenAI publicly confirmed it had filed confidential IPO paperwork with the SEC. The market read this as a reinforcement of the AI infrastructure story even with everything else going on, and it landed only a week after Anthropic’s own confidential filing.

Tuesday — A Helicopter, a 5% Drop, and a Recovery

Tuesday was the kind of session that tests discipline. Markets opened modestly higher, then fell sharply. Trump announced that Iran had shot down a U.S. Army Apache helicopter patrolling near the Strait of Hormuz (the U.S. military believes the helicopter was brought down by an Iranian Shahed drone, just off the coast of Oman; both pilots were recovered safely). U.S. Central Command later confirmed retaliatory strikes against Iran in response. The Nasdaq fell as much as 5.3% intraday before buyers stepped in aggressively off the lows, staging one of the more remarkable intraday recoveries in recent memory.

By the close, the Nasdaq finished down just under 1% — a result that would have seemed almost impossible at the session’s lows. It was one of the widest intraday ranges (peak-to-trough swing in a single trading day) we have seen in years, and a useful reminder of how headline-driven this market has become.

Wednesday — Hot CPI, More Strikes, and a Risk-Off Close

Tuesday’s reprieve did not last. The S&P 500 lost 1.62% and the Nasdaq dropped nearly 2% as Trump pledged more strikes on Iran and the May Consumer Price Index report (released by the Bureau of Labor Statistics Wednesday morning) gave investors nothing to hold on to. Headline CPI — the broadest measure of consumer prices — came in at 4.2% year-over-year, in line with expectations but the highest reading in three years. Core CPI, which strips out food and energy to show the underlying trend, was 2.9%. On the month, headline prices rose 0.5% and core rose 0.2%, just below the 0.3% economists expected.

The softer monthly core figure was the bright spot, but it was overwhelmed by the bigger picture: inflation remains well above the Fed’s 2% target, U.S. strikes on Iran resumed after Tuesday’s close, and oil climbed back above $90 a barrel. Concerns about AI stock valuations — simmering since Broadcom’s earnings the week before — added a third layer of pressure. Suddenly the next day’s producer price report was the most important data release of the week.

Thursday — Trump Cancels the Strikes

Thursday opened with Trump declaring on Truth Social that the U.S. would attack Iran “VERY HARD TONIGHT.” By that afternoon, the story had flipped completely. Trump announced he was canceling the planned strikes and said the two countries were close to a peace agreement, with a signing potentially as soon as this weekend. A source acknowledged real breakthroughs in Qatar-mediated talks that had run through the early morning hours, and Trump said discussions had been raised to the highest level of Iranian leadership and approved.

The Producer Price Index report (which measures prices businesses pay, and often previews where consumer prices are heading) landed in the middle of all of this. The read was mixed. Headline PPI came in hot at 6.5% year-over-year — above the 6.4% estimate, the highest reading since 2022 — and 1.1% on the month against a 0.7% expectation. Core PPI, however, was softer than expected: 4.9% year-over-year versus 5.4% expected, and 0.4% on the month versus 0.5%. The softer core read suggests price pressure deeper in the pipeline may be easing at the margin, even as headline numbers stay elevated — most of which traces back to oil and the disruption around the Strait of Hormuz. In a normal week the PPI surprise would have dominated the conversation. This was not a normal week.

Stocks staged a sharp reversal to the upside as the Iran peace signal overwhelmed everything else. Iran’s foreign ministry cautioned that no deal had been finalized, and the week’s pattern — escalation, peace signal, more escalation — left the durability of the rally an open question. But by the close the mood had clearly shifted.

Friday — SpaceX Makes History

Friday belonged to SpaceX. The company priced its IPO at $135 per share Thursday night and opened at $150 on Friday — an 11% pop right out of the gate. It closed up roughly 19% at $160.95, valuing the company above $2 trillion at the close. The total proceeds of about $75 billion make it the largest IPO in market history, dwarfing Saudi Aramco’s 2019 debut (roughly $25 billion). The sheer size of the deal pulled enormous liquidity into the stock and away from the rest of the tech complex, driving a rotation toward value and equal-weight names.

Crude oil eased on renewed Iran peace hopes, rate-sensitive sectors got some relief, and U.S. equities edged modestly higher on the day, with equal-weight and value-oriented names leading. A fitting end to the most chaotic week of 2026.

What We're Watching Next Week

Will the Iran peace deal hold?

This remains the single most important variable in the market. A signed deal would likely send oil materially lower, ease pressure on interest rates, and let the AI infrastructure trade reaccelerate. A breakdown would put us right back at $90-plus crude with a Fed that has no room to maneuver. Trump has described a signing as imminent; Iran’s foreign ministry has not yet confirmed a finalized agreement. We have seen this pattern before, so we will believe it when we see it.

The Fed decision and Warsh’s first press conference (Wednesday, 2:30 PM ET)

No rate change is expected, but the statement and press conference may matter more than any decision in recent memory. This is Kevin Warsh’s first press conference as Fed Chair (he was sworn in May 22), and investors will be parsing every word for signals about whether he is leaning more neutral or more hawkish. Warsh has previously suggested he wants to overhaul how the Fed communicates with markets — including potentially reducing the frequency of press conferences, changing forward guidance (the Fed’s practice of signaling where rates are headed next), and reworking the quarterly dot plot (the chart showing where each policy maker individually expects rates to go). Any meaningful changes to that communication framework would be a real structural shift in how Wall Street interprets the Fed. Combined with Wednesday’s CPI print and Thursday’s hot PPI headline, Warsh has very little room to sound dovish, and the market knows it.

SpaceX (SPCX) follow-through

Whether the IPO enthusiasm sustains, or SPCX continues to pull capital out of the rest of the tech complex, will matter for how the broader market trades next week. We are actively evaluating SPCX for potential inclusion in our strategies and will communicate any decisions through our normal channels.

Treasury yields and the oil-and-rates link

A finalized Iran deal and a meaningful drop in crude would do a lot of the Fed’s inflation work for it. The 10-year Treasury yield’s reaction to any resolution will be one of the cleanest reads on where rate expectations are heading. One data point worth keeping in mind as you watch yields next week: the 3-month rolling correlation between the 10-year yield and the S&P 500 has fallen to -0.62. In plain English, stocks and bonds are moving in opposite directions more strongly than they have in at least 15 years — worse than anything we saw during the 2022 bear market. Right now, when yields go up, stocks go down. And because this is being driven by inflation fear rather than growth fear, the usual “bad economic news is good for stocks” reflex does not apply. A peace deal that pulls oil lower would relieve that yield pressure and remove one of the biggest mechanical headwinds the equity market is facing right now.

The Bigger Picture

SpaceX’s public debut is a landmark moment for the AI infrastructure cycle. A company that owns the world’s most advanced satellite network, has absorbed xAI, and went public at roughly a $2 trillion valuation is a statement about where capital is flowing and what investors are willing to pay for durable infrastructure sitting at the intersection of space, connectivity, and artificial intelligence.

But the AI and growth leadership that carried markets through the spring came under real pressure again this week. The aggressive selling that started last Friday carried straight into Tuesday and Wednesday, with semiconductors and high-multiple software names taking the brunt of it. Geopolitical risk-off, a hot inflation print, and valuation fatigue all hit the most crowded trades at once. The late-week rebound, once Thursday’s peace signal landed, was instructive: the structural demand for AI infrastructure has not gone away, but the market delivered a clear reminder that stretched valuations leave very little room for macro surprises. When everything goes wrong at once — oil spikes, CPI runs hot, a helicopter gets shot down, and the new Fed Chair signals a communication overhaul — the most expensive stocks absorb the most pain. When the skies clear, even briefly, those same stocks recover first. That asymmetry cuts both ways, and it is exactly why trimming into strength and keeping cash on hand matters.

What this week showed, taken together, is that the AI bull market is not immune to the world around it. Four months of conflict, a partially closed Strait of Hormuz, 4.2% headline CPI, a PPI surprise, and a Fed leadership change with real policy uncertainty are not trivial headwinds. They are exactly why we have been trimming winners, raising cash, and rotating into better risk-reward setups rather than simply holding through the noise.

The 5% intraday drop and recovery we saw Tuesday do not happen often, and they are not comfortable to live through. What we can tell you is that we were active and engaged all week — raising cash when we needed to, adding when the opportunity showed up, and making every move with your long-term outcome in mind. Volatility is not a reason to abandon a well-built portfolio — it is the environment in which a well-built portfolio earns its keep.

If you ever want to walk through how your portfolio is positioned, please reach out. That is exactly what we are here for.

This market update is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

Our Form ADV Part 2, which describes our services, fees, conflicts of interest, and advisory practices in detail, is available at Form ADV Part 2 and at www.adviserinfo.sec.gov.

Educational content only. This article is for informational and educational purposes and does not constitute investment advice or a recommendation of any specific strategy or service. All references to AI tools describe general capabilities of technology in the financial services industry; they do not represent performance guarantees or specific results for any client. Past performance is not indicative of future results. Investing involves risk, including possible loss of principal. Neptune Advisory LLC (d/b/a Neptune Wealth) is a Registered Investment Adviser in Pennsylvania, Florida, and Wisconsin.. Please review our Form ADV Part 2 before engaging our services.