Weekly Market Update: May 18–22, 2026

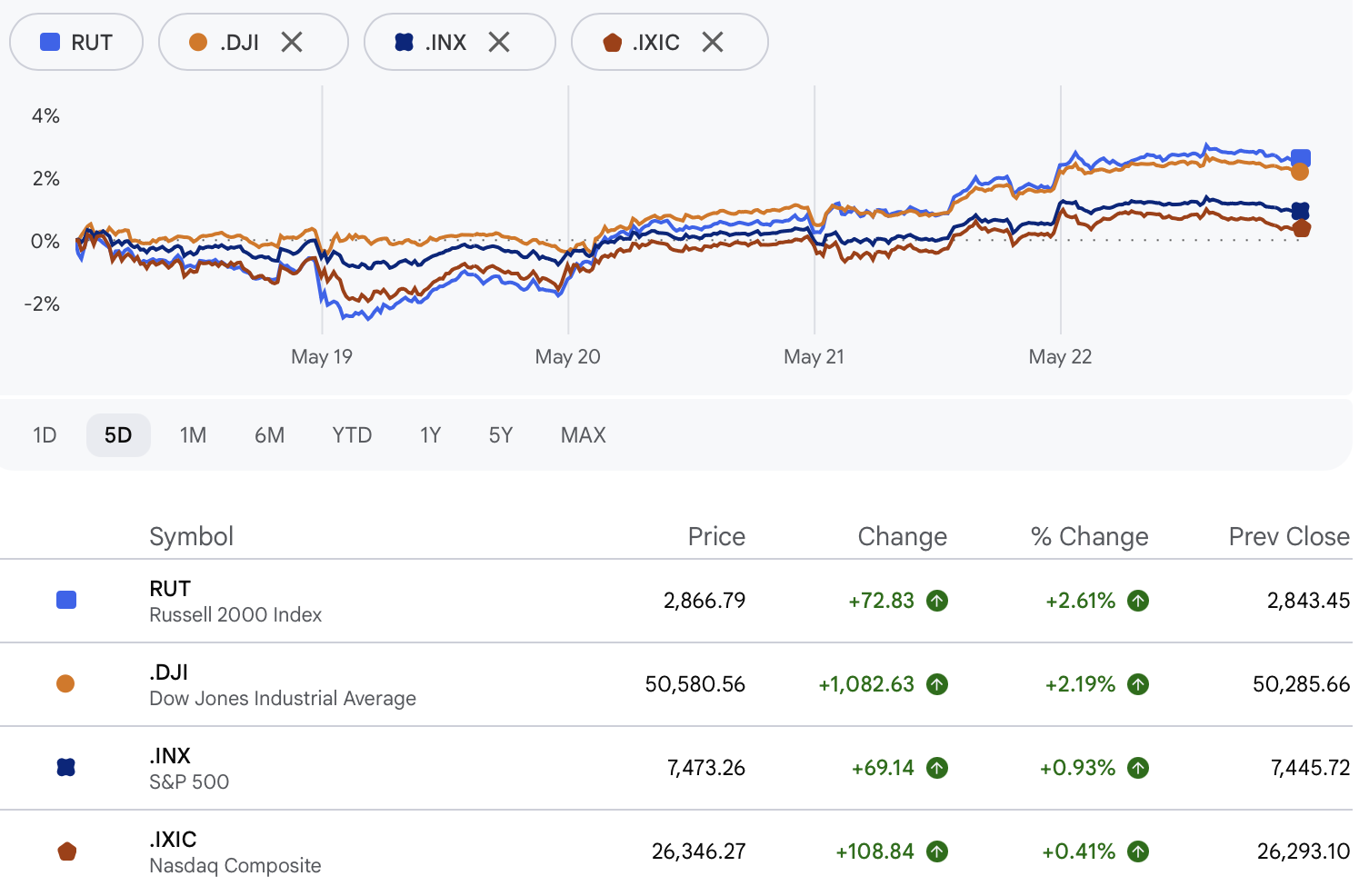

This week tested the market's conviction as investors weighed exceptional AI earnings against rekindled inflation fears and the “higher for longer” interest rate narrative. Stocks came under pressure early as Treasury yields spiked on renewed inflation fears and broader risk-off sentiment. Sentiment recovered sharply mid-week after Nvidia delivered another blowout quarter, reinforcing confidence in the AI buildout — and Wednesday's FOMC minutes, confirming a majority of policymakers favor additional hikes if inflation stays elevated, were largely absorbed without further damage. Yields eased into the back half of the week, and progress on a U.S.–Iran deal provided additional tailwind into Friday. The week's takeaway: a market still willing to reward growth, but increasingly sensitive to rates and the weight of its own expectations.

What Happened This Week

Monday — Risk-Off to Start

Tech and growth names sank to open the week as the 10-year Treasury yield hit its highest level in more than a year, spooking the rate-sensitive growth names that have powered much of the rally. Geopolitical pressure around the Strait of Hormuz kept oil elevated and sent investors into defensive positioning. Broad indices largely clawed back their losses by end of day — but growth names weren't so lucky, finishing the session meaningfully in the red.

Musk v. Altman — Verdict in OpenAI's Favor

A San Francisco jury threw out Elon Musk's lawsuit against OpenAI in under two hours, ruling he had waited too long to sue and finding OpenAI, Sam Altman, and co-founder Greg Brockman not liable on all counts. Musk was quick to condemn the verdict, calling it a "calendar technicality" and arguing that the judge and jury never ruled on the actual merits of the case. He has vowed to appeal to the U.S. Court of Appeals for the Ninth Circuit — this fight is not over. For markets, the immediate read is that OpenAI emerges with its momentum intact and one fewer near-term distraction on its path to the public markets.

Tuesday — Yields Spike, Inflation Fears Reignite

The 10-year reached its weekly high as rekindled inflation fears drove a continued selloff in Treasuries, pressuring rate-sensitive equities further. With no major catalyst to offset the move, the session was defined largely by the yield spike itself — a reminder that the macro backdrop remains a live risk even when earnings are cooperating. The pressure was broad-based, with growth names bearing the brunt.

Wednesday — Nvidia Delivers, FOMC Minutes Absorbed, Markets Recover

Nvidia reported Q1 FY27 results that were, by any objective measure, extraordinary. Revenue hit a record $81.6 billion, up 85% year-over-year, well ahead of the $78.75 billion consensus. Data Center revenue reached $75.2 billion, up 92%. Non-GAAP EPS of $1.87 beat estimates of $1.70. CEO Jensen Huang closed the call simply: "Demand has gone parabolic. The reason is simple: Agentic AI has arrived." The company guided Q2 to $91 billion, raised its quarterly dividend 25x, and added $80 billion to its buyback authorization.

Also Wednesday, the FOMC minutes confirmed what the market had been suspecting: a majority of policymakers believe additional rate hikes may be warranted if inflation stays persistently above target. It was a hawkish read — but with Nvidia's results dominating the narrative, the minutes were largely absorbed without further damage. The Nasdaq gained 1.54%, the S&P 500 added 1.08%, and the Dow reclaimed 50,000.

Thursday — Sell the News, Beneficiaries Stay Green

Despite the blowout print, Nvidia shares fell Thursday as guidance didn't reach the upper end of the most aggressive whisper numbers. More interesting: indirect AI infrastructure beneficiaries across cloud, power, and data center supply chain continued to catch bids — exactly the rotation we've been positioning around. Thursday afternoon also brought reports that a U.S.–Iran deal draft, mediated by Pakistan, was near announcement, with Secretary Rubio acknowledging "some good signs." Oil pulled back, and markets continued to rally into the close.

Friday — Yields Ease, Sentiment Stabilizes

The 10-year eased to roughly 4.55% — its lowest of the week — as Iran deal optimism helped oil retreat and temporarily reduced inflation expectations. The situation remains fragile: Iran's Supreme Leader hardened Tehran's position on a key U.S. demand, and nothing is done until it's done. But the direction of travel improved heading into the weekend, and the S&P 500 and Nasdaq finished the week in positive territory once again.

What We're Watching Next Week

Thursday's data slate is the week's focal point — three reports dropping together:

- Core PCE MoM: The Fed's preferred inflation gauge. A hot number would cement the "no cuts in 2026" narrative; a softer read could provide real relief.

- GDP Growth Rate QoQ: The Q1 revision tells us whether the economy can still absorb higher rates — or whether cracks are forming.

- Personal Income and Spending MoM: Consumer spending has been the economy's ballast. Any softening here, against elevated energy costs and higher borrowing rates, would matter.

Beyond the data: the U.S.–Iran situation remains a live variable for oil and inflation. And elevated Treasury yields will continue to be the key signal for equity multiples — stability there creates room for growth names to breathe; a renewed push higher would be a headwind.

The Bigger Picture

The market is holding up remarkably well against several headwinds. Yields are elevated, the Fed is leaning hawkish, and geopolitical risk looms. And yet earnings — led again by Nvidia — keep coming in above expectations, AI capital expenditure is accelerating, and the equity market has not broken down. That tension between strong fundamentals and a challenging rate environment is likely to define the months ahead.

As we monitor yield fluctuations, it becomes important to assess the interplay with the AI momentum trade. AI-driven investments continue to captivate market attention, but we recognize that momentum of this magnitude decelerates eventually — and if yield pressures persist, a strategic pivot may be necessary to maintain balance.

Additionally, today's confirmation of Kevin Warsh and the implications for the Federal Reserve's stance on inflation and monetary policy adjustments are crucial elements to consider. These developments form part of the broader economic puzzle that will inform our decisions moving forward. As always, please reach out with any questions about how these developments may affect your portfolio.

This market update is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

Our Form ADV Part 2, which describes our services, fees, conflicts of interest, and advisory practices in detail, is available at Form ADV Part 2 and at www.adviserinfo.sec.gov.

Educational content only. This article is for informational and educational purposes and does not constitute investment advice or a recommendation of any specific strategy or service. All references to AI tools describe general capabilities of technology in the financial services industry; they do not represent performance guarantees or specific results for any client. Past performance is not indicative of future results. Investing involves risk, including possible loss of principal. Neptune Advisory LLC (d/b/a Neptune Wealth) is a Registered Investment Adviser in Pennsylvania, Florida, and Wisconsin.. Please review our Form ADV Part 2 before engaging our services.