Weekly Market Update: May 11 - May 15, 2026

The week was defined by two inflation shocks, a high-stakes diplomatic summit, and a Friday sell-off that erased much of the mid-week recovery. Back-to-back CPI and PPI prints surprised meaningfully to the upside on Tuesday and Wednesday, before a rebound on Trump–Xi summit optimism gave investors some footing. Friday gave it back: a global bond sell-off sent the 10-year Treasury yield to ~4.60% and the 30-year past 5.12% as inflation fears, higher oil prices, and rising odds of a Fed hike overwhelmed any diplomatic goodwill. Market expectations for a 2026 rate cut effectively collapsed to zero. It was a week where macro headlines mattered more than anything happening at the company level.

What Happened This Week

Tuesday — CPI Shock Triggers Broad Sell-Off

April CPI delivered a significant upside surprise. Headline CPI rose 0.6% on the month, pushing the annual rate to 3.8% — the highest since May 2023 and a half-point jump from March. Core CPI rose 0.4% on the month and 2.8% year-over-year, confirming that underlying price pressures remain persistent. Energy was the principal driver, with the energy index up 17.9% year-over-year (the steepest annual increase since September 2022), gasoline +28.4%, and fuel oil +54.3%.

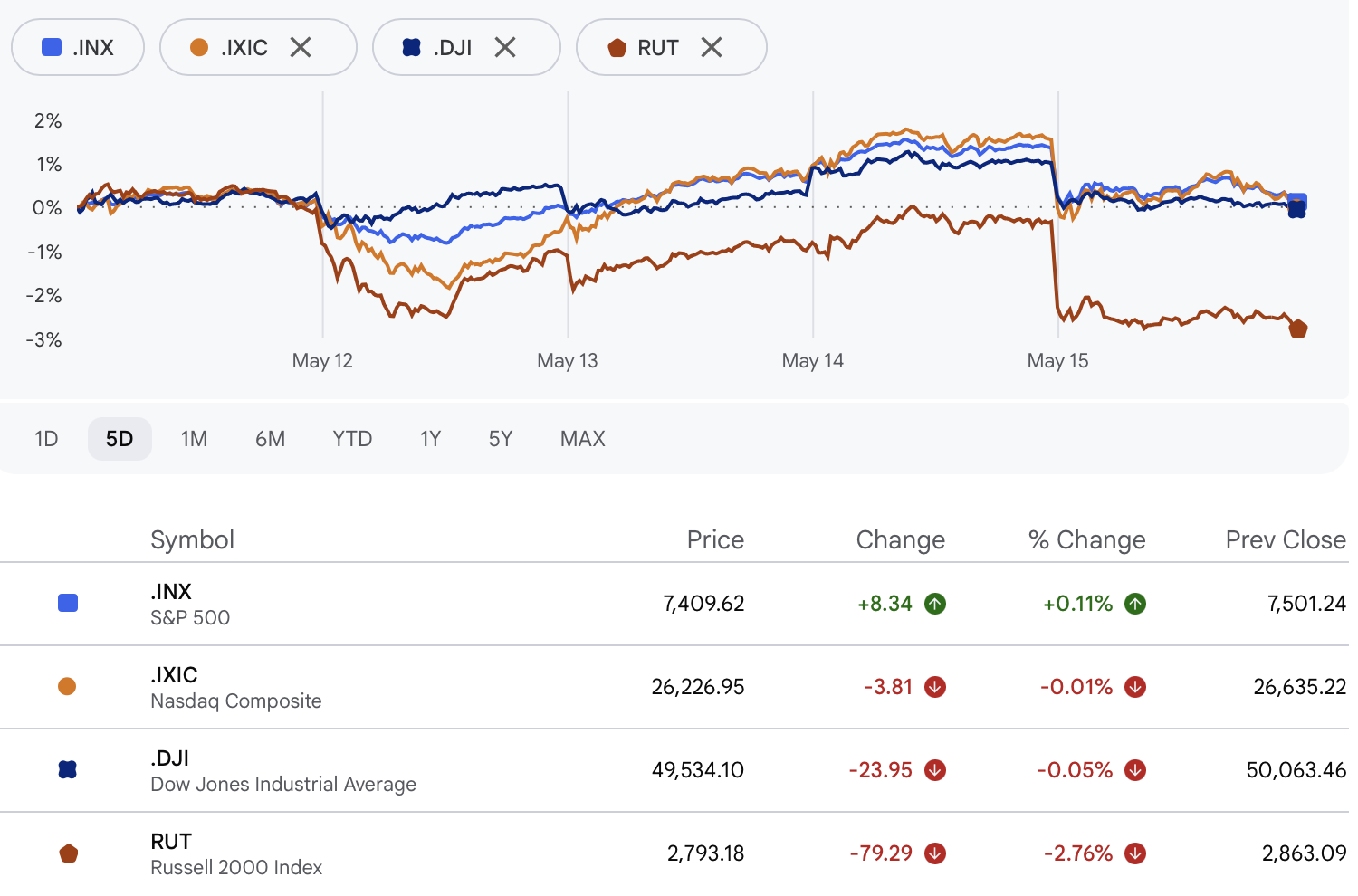

The data triggered an immediate, broad-based sell-off. All three major indexes fell sharply, with rate-sensitive growth names absorbing the most pain. Treasury yields spiked across the curve as investors rapidly repriced the likelihood of near-term Fed easing.

Wednesday — PPI Piles On, Then Markets Find Their Footing

Wednesday's PPI compounded the concern. April PPI advanced 1.4% on the month — well above the 0.5% Dow Jones consensus and the largest monthly increase since March 2022 — with the annual rate jumping to 6.0% (the biggest year-over-year gain since December 2022). Core PPI accelerated 1.0% on the month versus the 0.4% estimate, lifting the annual core rate to 5.2%. Notably, services prices rose 1.2%, with two-thirds of the move attributed to a 2.7% rise in trade services — an early sign that tariff costs may be filtering more broadly into the price chain.

Despite the back-to-back shocks, markets staged a meaningful recovery into Thursday as investors looked toward the Trump–Xi summit in Beijing, interpreting a potential diplomatic reset with China as a possible source of supply-side relief. The rally clawed back a significant portion of Tuesday's losses — before Friday reversed course.

The Trump–Xi Summit

President Trump's visit to Beijing — the most significant foreign trip of his second term — wrapped on Friday without major breakthroughs, but with enough positive optics to give markets something to rally around mid-week. Trump was received with pageantry by President Xi Jinping, though the warmth was offset by unresolved tensions on several fronts.

The central issue was Iran. The U.S. has pressed Beijing to lean on Tehran to reopen the Strait of Hormuz, but China's official readouts barely mentioned it. Trump told reporters he was not asking Xi for "favors," suggesting Xi would "automatically" pressure Tehran — language that left markets with little certainty about Beijing's intentions.

On trade, Xi signaled China's economic door would "only open wider," and Trump said China had agreed to purchase 200 Boeing jets — above the 150 the company had expected, but well short of the 500 some had initially anticipated. Beijing raised Taiwan as "the most important issue in China–U.S. relations," warning that mishandling it could put the relationship in "great jeopardy." The summit's one concrete outcome: Xi accepted Trump's invitation to visit the U.S. in September. Elon Musk, Tim Cook, and Jensen Huang accompanied the delegation, underscoring the commercial stakes.

For markets, the summit's ambiguity was treated as a modest positive through Thursday — the absence of escalation being preferable to confrontation — and it provided the catalyst for the mid-week recovery off Tuesday's inflation-driven lows.

Friday — Treasury Yields Surge, Rate Cuts Off the Table

Friday was the week's most difficult session, driven less by the summit and more by an alarming bond-market development. The 10-year yield climbed to approximately 4.60% and the 30-year broke above 5.12% — its highest since 2007. That kind of move reprices virtually every asset on the board. Four forces converged to drive the spike:

- Hotter-than-expected inflation: April CPI and PPI both surprised to the upside, stoking fears that a "second wave" of inflation could be becoming entrenched.

- Surging energy costs: Escalating tensions in the Middle East — specifically around the Strait of Hormuz — pushed crude prices meaningfully higher, reinforcing the inflation narrative.

- Rising rate expectations: Traders dramatically increased the probability that the Fed will hike rates before year-end rather than cut. Expectations for a 2026 cut have effectively collapsed to zero, with some investors now pricing in hikes — a sharp pivot from just a month ago, when one to two cuts in the back half of 2026 were the base case.

- Global bond sell-off: The pressure was not confined to the U.S. — Japanese yields surged to multi-decade highs on a jump in wholesale inflation, while U.K. Gilt yields rose on political uncertainty. The synchronized global sell-off amplified domestic pressure and removed a potential safe-haven offset.

The equity damage was broad but uneven. The Russell 2000 bore the brunt, falling nearly 3% on the week as smaller-cap names proved most sensitive to tightening financial conditions. The S&P 500 managed a fractional weekly gain of +0.11% and the Nasdaq closed essentially flat at -0.01% — outcomes that reflect the mid-week relief rally more than any underlying strength on Friday.

What We're Watching Next Week

- Retail earnings (Tue–Thu): Home Depot (Tuesday, May 19), Target and Lowe's (Wednesday, May 20), and Walmart (Thursday, May 21) will give a real-time read on the U.S. consumer just as inflation and rate fears resurface.

- Nvidia earnings (Wednesday, May 20): Nvidia's FY27 Q1 results will likely dictate the next move for the AI-driven technology rally. Consensus is ~$1.78 EPS on $78.98B revenue. Investors will scrutinize data-center revenue, margins, and forward guidance on hyperscaler demand. A strong print could reignite the AI infrastructure trade; a miss or cautious outlook could weigh on the entire sector.

- FOMC Minutes (Wednesday, May 20): The minutes will be closely parsed for insight into how the committee was thinking about inflation before last week's hot data. Any language around rate-cut conditions will carry added weight — and could move bond markets if the bar for easing was already being raised.

- Iran/Hormuz: Negotiations on a formal ceasefire continue. The Strait remains a pressure point, and any escalation or breakthrough will move oil prices and risk assets quickly.

Treasury yields: After Friday's spike, bond-market stability will be important for equity-multiple support heading into the week. Continued pressure on yields would be a headwind, particularly for longer-duration growth names.

The Bigger Picture

This was not the week anyone was hoping for on the inflation front. The CPI and PPI prints were unambiguous: price pressures are not cooling at the pace the Fed needs to justify easing, and the market has been forced to dramatically revise its rate expectations — from cuts priced in, to no movement, to whispers of hikes.

And yet, the equity market's mid-week recovery is telling. With geopolitical uncertainty elevated and inflation running hot, markets still found a reason to rally in the absence of outright catastrophe. The Trump–Xi meeting produced no landmark agreements, but it did not blow up — and for a market navigating a challenging macro environment since February, that was enough.

Don't fight the Fed. Strong corporate earnings and an accelerating AI buildout are running headlong into a more stubborn inflation environment than anyone hoped — and a Fed that may have less room to ease than markets had priced. We continue to manage risk carefully, stay selective in new positioning, and hold to a thesis built on fundamentals rather than rate-cut forecasts. As always, please reach out with any questions about how these developments may affect your portfolio.

This market update is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

Our Form ADV Part 2, which describes our services, fees, conflicts of interest, and advisory practices in detail, is available at Form ADV Part 2 and at www.adviserinfo.sec.gov.

Educational content only. This article is for informational and educational purposes and does not constitute investment advice or a recommendation of any specific strategy or service. All references to AI tools describe general capabilities of technology in the financial services industry; they do not represent performance guarantees or specific results for any client. Past performance is not indicative of future results. Investing involves risk, including possible loss of principal. Neptune Advisory LLC (d/b/a Neptune Wealth) is a Registered Investment Adviser in Pennsylvania, Florida, and Wisconsin.. Please review our Form ADV Part 2 before engaging our services.