The Backdoor Roth IRA: A 2026 Guide for High-Income Earners

The Roth IRA is one of the most attractive retirement vehicles in the U.S. tax code: contributions grow tax-free, qualified withdrawals in retirement are not taxed, and there are no required minimum distributions during the owner's lifetime. The catch is that Congress attached income limits to it. Once your modified adjusted gross income climbs past the threshold, you cannot contribute directly.

The backdoor Roth IRA is a two-step workaround that sidesteps those income limits entirely. It is not a loophole in the shadowy sense — Congress explicitly removed the income cap on pre-tax IRA to Roth IRA conversions in 2010, and the IRS has repeatedly acknowledged the strategy. Here is how it works in 2026, what thecurrent numbers are, and where people trip up.

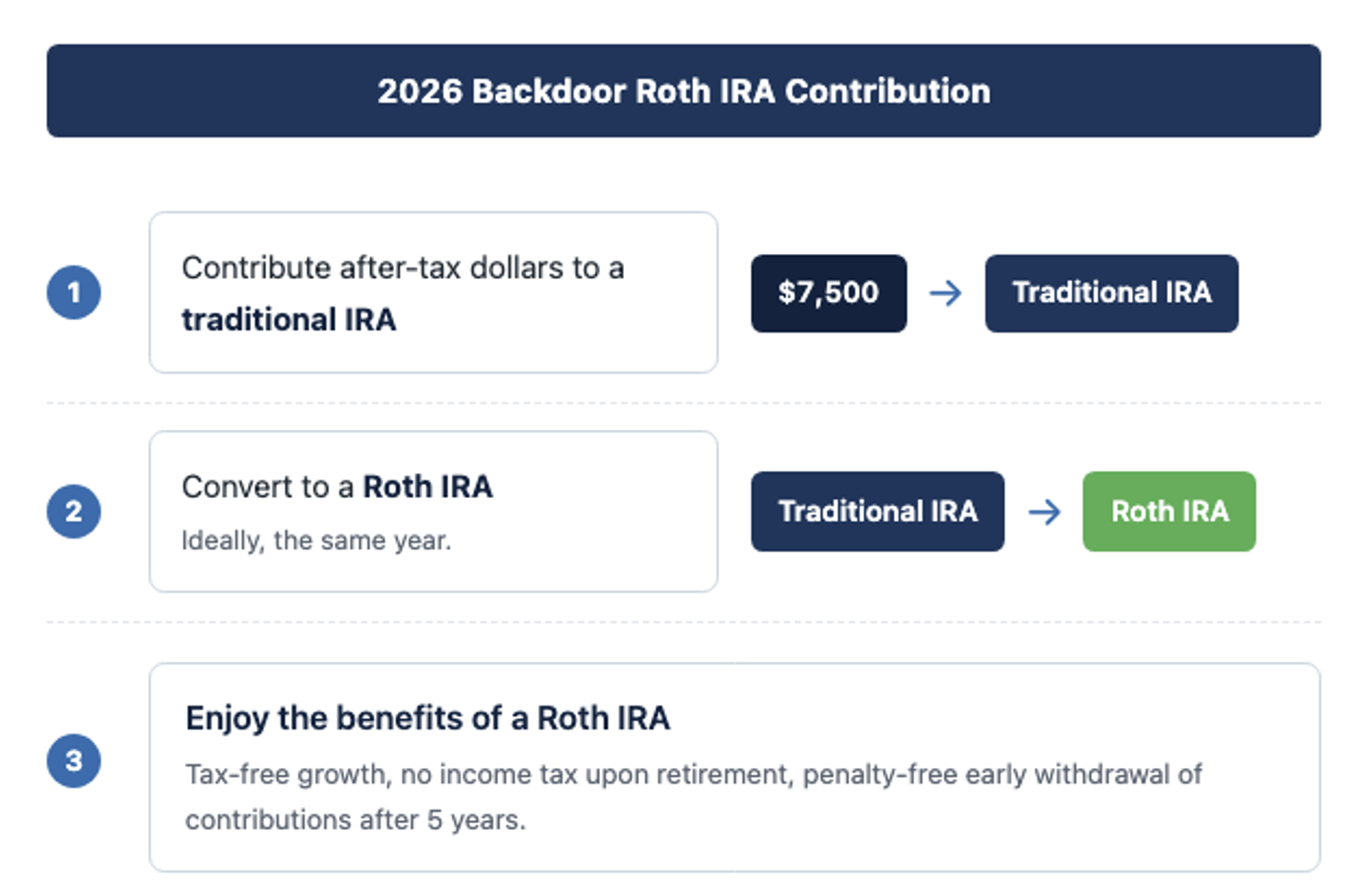

The three-step strategy at a glance

Why a backdoor is needed in the first place

Direct Roth contributions are phased out based on modified adjusted gross income (MAGI). For 2026, the IRS-announced ranges are:

Once you are above the upper end of the range, you cannot make a direct Roth contribution. But the law places no income limit on (a) making a nondeductible contribution to a traditional IRA, or (b) converting a traditional IRA to a Roth. Chaining those two steps together is the backdoor Roth.

Step 1: Make a nondeductible contribution to a traditional IRA

For 2026, the contribution limit across all your IRAs is $7,500 (or $8,600 if you are age 50 or older). Unlike the base contribution limit, which has long been indexed to inflation, the $1,100 catch-up amount is a newer development — SECURE 2.0 made the catch-up limit inflation-adjustable starting in 2024, and 2026 marks the first year it increased, from $1,000 to $1,100.2

Because your income is high enough that you are reading this article, odds are your traditional IRA contribution will not be deductible — either because you are covered by a work place plan and phased out, or because your spouse is. That is fine. In fact, it is the whole point: you want the contribution to land in the IRA with an after-tax basis, so that when you convert it, there is nothing new to tax.

The nondeductible contribution and conversion is reported on IRS Form 8606, which establishes your basis. This is the single most skipped step in the entire strategy, and it creates real problems years later if missed.

Step 2: Convert to a Roth IRA

Roth conversions are governed by IRC § 408A(d)(3), which in 2010 removed the old $100,000 MAGI cap on conversions. There is no income limit, no dollar limit, and no waiting period — you can convert the day after contributing.

If the traditional IRA holds only your fresh nondeductible contribution and has not earned anything meaningful before you convert, the conversion is essentially tax-free: you already paid tax on the money, and there are no pre-tax dollars to recognize as income.

Step 3: Let it grow, tax-free

Once in the Roth, the money grows tax-free and qualified distributions come out tax-free.3 Two details high earners should know:

The 5-year rule on conversions

Each Roth conversion starts its own 5-year clock. If you withdraw the converted principal within 5 years and you are under age 59½, the 10% early-withdrawal penalty under IRC §72(t) can apply — even though you already paid tax on the dollars at conversion. After five tax years (measured from January 1 of the conversion year), the converted principal can come out penalty-free.4

The 5-year rule on earnings

Separately, for the earnings on your Roth to come out entirely tax-free, you must be age 59½ and have had any Roth IRA open for at least 5 tax years.5 The two 5-year rules are distinct and frequently confused.

Who should consider this?

The backdoor Roth is most useful for people who: (1) earn above the direct-Roth phase-out, (2) have little or no pre-tax balance in traditional, SEP, or SIMPLE IRAs (or are willing to roll those into a 401(k) first), and (3) already max their workplace retirement plan and want additional tax-advantaged space.

If you can contribute to a Roth directly, do that — it is simpler, and you do not need Form 8606. If you are near the phase-out, run the MAGI math carefully; partial contributions are allowed inside the phase-out range.

Common mistakes

Skipping Form 8606. This form is how you prove to the IRS that you already paid tax on the money you contributed. Skip it, and that record disappears — leaving you vulnerable to paying tax on the same money again when you withdraw it later.

Losing your basis when you switch tax software or accountants. Form 8606 tracks your cumulative after-tax basis on line 14, and that number must roll forward on every return for as long as your IRA carries basis. The problem is that this figure doesn't always travel with you when you change software or hire a new CPA.

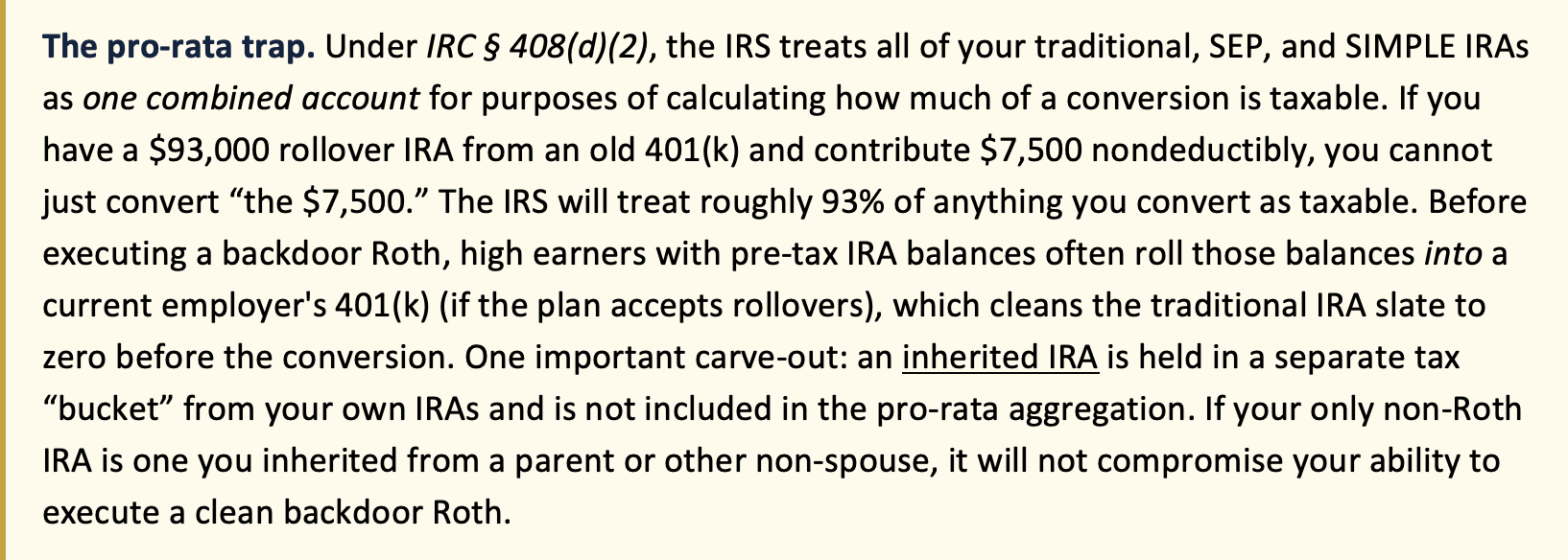

Mistiming a rollover. The IRS calculates the pro-rata rule using your total IRA balance on December 31 of the conversion year — not the day you complete the conversion. That timing detail can catch people off guard.

Here's how it can play out: In January 2025, you contribute $7,000 to a traditional IRA and convert it to a Roth the very next day. At that point, everything looks fine — your IRA is empty and the conversion should be tax-free. But in December, you change jobs and roll your old pre-tax 401(k) into a traditional IRA. Your IRA balance on December 31 is now $93,000.

When you file your 2025 return, Form 8606 calculates the taxable portion of your conversion using a simple fraction: your after-tax basis divided by your total December 31 IRA balance plus the amount you converted. In this case, that's $7,000 divided by $100,000 ($93,000 + $7,000), which means only 7% of your conversion is tax-free. The remaining 93%, or $6,510, is treated as taxable income on your 2025 return. A conversion you thought was clean in January turned into a surprise tax bill in April.

The takeaway: if you're planning a backdoor Roth conversion, be very careful about rolling pre-tax money — like an old 401(k) — into a traditional IRA in the same calendar year. The rollover doesn't have to happen before the conversion to cause a problem. It just has to happen before December 31.

Waiting too long between steps. Any earnings that accrue in the traditional IRA between contribution and conversion are taxable when converted. Most people convert within a few days to keep that number at or near zero.

Assuming the strategy is guaranteed forever. Legislators periodically propose closing the backdoor Roth for high earners. It is open in 2026, but that is a political decision that could change in future tax years.

Allowing tax to be withheld from your distribution. When you take money out of a traditional IRA to convert it to a Roth, your custodian may offer — or in some cases default — to withhold a portion for taxes, typically 10%. This might seem convenient, but it creates a problem. Only the amount that actually arrives in your Roth IRA counts as being where converted. The withheld portion is treated as a distribution, meaning it's subject to income tax and, if you're under 59½, a 10% early withdrawal penalty on top of that. To avoid this, always elect zero withholding when processing a conversion and plan to cover any tax bill from money outside the IRA. A conversion should be a direct movement of the full balance — not a net check after taxes are skimmed off the top.

Bottom line

For a high-income earner in 2026, the backdoor Roth is still one of the cleanest ways to get an extra $7,500 (or $8,600 if age 50+) into a tax-free retirement bucket every year. Mind the pro-rata rule, file your Form 8606, and respect the 5-year clocks, and the strategy is as simple as its three-step diagram suggests.

This article is for informational purposes only and is not tax or legal advice. Before executing a backdoor Roth — particularly if you hold pre-tax IRA balances — consult a CPA or tax advisor familiar with your situation.

Sources

1. IRC § 408A(c)(3) (Roth IRA MAGI phase-out ranges); IRS Notice 2025-67 (2026 cost-of-livingadjustments).

2. IRC § 219(b) (IRA contribution limit); IRC § 408A(c)(2) (Roth contributions cannot exceed §219(b) limit); IRS Notice 2025-67.

3. IRC § 408A(d)(2) (definition of qualified distributions from a Roth IRA).

4. IRC § 408A(d)(2)(B) (five-year holding requirement); IRC § 72(t)(2)(F) (10% additional tax and its application to recently converted amounts).

5. IRC §408A(d)(2)(A)–(B) (age-59½ and five-year requirements for tax-free treatment ofRoth earnings).

About the Author:

Mark Strey has been helping high-income clients navigate complex financial decisions since 2013. In addition to being a CFP® professional, he holds a Master of Taxation from Villanova University's Charles Widger School of Law and is authorized to practice before the IRS as an Enrolled Agent. At Neptune Wealth, Mark combines deep tax expertise with comprehensive wealth management to help clients build and protect long-term wealth.