Market Update: April 13 - April 17, 2026

This was another remarkable week — and a positive one. Let us walk you through what happened, how we positioned portfolios, and what we're focused on heading into next week.

As always, we've broken this summary into focused sections — feel free to read it in full or jump to what's most relevant to you.

What Happened This Week

Markets closed higher for the third consecutive week, capping what can only be described as one of the most consequential reversals in recent memory. All four major indexes surged, with breadth improving meaningfully and several indices hitting levels not seen in months. The spark was geopolitical — but the fuel was something that had been building beneath the surface for weeks.

Weekly returns across the major indices:

- S&P 500: Surpassed the 7,100-point mark for the first time on Friday

- Nasdaq: Extended its winning streak to 13 consecutive sessions — the longest run since 1992

- Dow Jones: Reached its highest level in over two months, driven by broad participation

- Russell 2000: Also achieved new record highs, a meaningful sign that this rally is not concentrated at the top

The combination of easing geopolitical tensions, plummeting oil prices, and strong early corporate earnings created a powerful backdrop for risk assets this week. Investors who stayed the course through the volatility are now seeing that patience rewarded in a very real way.

Sunday Night Shock — Then Monday's Resilience

Before we get to the week's resolution, it's worth acknowledging how it began. On Sunday, April 13th, President Trump announced that the U.S. Navy would blockade the Strait of Hormuz after ceasefire talks ended without a final agreement. It was a significant escalation in tone — one that, just weeks ago, might have sent futures sharply lower and triggered a cascade of fear-based selling.

Instead, markets opened higher on Monday. Oil prices rose on the news, as one would expect, briefly trading above $100 per barrel. But the equity market's resilience in the face of that headline was itself a statement — a signal that the underlying bid beneath this market is real, and that investors are increasingly looking through near-term geopolitical turbulence toward a resolution they believe is coming.

That resilience set the tone for everything that followed.

Friday's Defining Moment — The Strait of Hormuz Opens

The defining headline of the week came Friday morning: Iran announced that the Strait of Hormuz is fully open. This development, combined with a 10-day ceasefire between Israel and Lebanon taking hold and President Trump welcoming Iran's announcement — while affirming that U.S. naval vessels will remain in place until a final U.S.-Iran peace deal is negotiated — represented a meaningful and concrete step toward resolution.

The market's reaction was immediate. WTI crude fell over 10% on Friday, dropping back below $90 per barrel — a significant relief valve for inflation expectations, transportation costs, and consumer spending. As Politico noted this week, the broader energy landscape is undergoing a structural shift as a result of this conflict: supply chains are being rewired, new energy partnerships are forming, and the world's relationship with Middle Eastern oil is being permanently recalibrated. The reopening of the Strait does not undo those changes overnight, but it is a critical pressure release that the global economy needed.

President Trump's response was characteristically firm — welcoming the move while making clear the U.S. would not fully stand down until a comprehensive deal is in place. That posture matters. It signals the administration wants a durable resolution, not a temporary one — and markets interpreted it as such.

What Drove the Magnitude of the Rally

It's worth being precise about the mechanics behind this week's move, because understanding why markets move the way they do is as important as tracking that they moved.

The primary driver was genuine fundamental optimism — falling oil prices reducing inflation risk, geopolitical de-escalation reducing the systemic risk premium that has been embedded in equities for weeks, and strong early earnings validating the growth thesis.

A contributing factor was short covering. Hedge funds have been closing short positions at the fastest pace since 2020, and as optimism built through the week, that mechanical buying added fuel to an already moving fire. It is important to understand the distinction: short covering can amplify a rally, but it does not create one. The foundation of this week's move was real.

Banking sector earnings early in the week also came in constructively, adding a further layer of confidence that the underlying economy, while not without stress, continues to function.

The Bigger Picture

Three weeks ago, we were in the middle of a multi-week losing streak with no clear end in sight. Today, we have three consecutive weeks of gains, indices at or near record highs, oil prices meaningfully off their peaks, and a geopolitical situation that — while not resolved — is moving in a constructive direction for the first time since February.

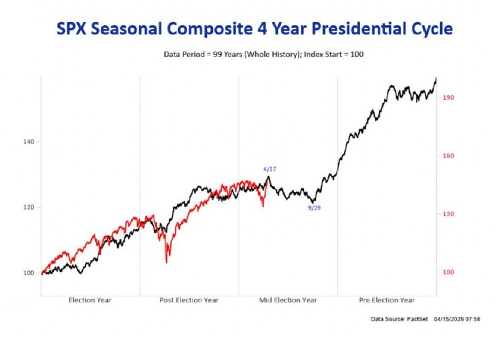

It is worth noting that 2026 is a midterm election year. Despite the extraordinary geopolitical backdrop, market performance this year has, in many respects, been tracking historical midterm-year patterns — as the FactSet data we’ve shared with you illustrates.

We understand that after significant run-ups, pullbacks are common. We remain bullish over the long term and are committed to adjusting our positioning as conditions evolve. Headline risk remains elevated — what the market rewards one day can fall out of favor quickly.

There is still meaningful uncertainty ahead. The ceasefire is only 10 days old, a final U.S.–Iran deal remains unsigned, and oil — while sharply lower — has not fully retreated. But the direction of travel has changed, and that matters. The positions we have been building are beginning to reflect the thesis we have held throughout this entire stretch, and we are encouraged by what we see ahead.

As always, please don't hesitate to reach out with any questions, or if you'd simply like to talk through your individual situation. That is what we are here for.

This market update is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

Our Form ADV Part 2, which describes our services, fees, conflicts of interest, and advisory practices in detail, is available at Form ADV Part 2 and at www.adviserinfo.sec.gov.

Educational content only. This article is for informational and educational purposes and does not constitute investment advice or a recommendation of any specific strategy or service. All references to AI tools describe general capabilities of technology in the financial services industry; they do not represent performance guarantees or specific results for any client. Past performance is not indicative of future results. Investing involves risk, including possible loss of principal. Neptune Advisory LLC (d/b/a Neptune Wealth) is a Registered Investment Adviser in Pennsylvania, Florida, and Wisconsin.. Please review our Form ADV Part 2 before engaging our services.